3 Stocks Im Watching This Month

Here are three companies I’m watching as we head into July—and why each one stands out.

I rely on Koyfin as a core part of my investment research. It’s a powerful platform for tracking markets, analyzing fundamentals, and building custom charts—all in one place.

Try Koyfin now and get 20% off any paid plan.

Each month, I highlight a few stocks that have earned a spot on my radar—sometimes because the business is evolving, sometimes because the price is.

To be clear: this isn’t a buy list.

If you’ve followed me for a while, you know I run a concentrated portfolio and don’t make moves lightly. I prefer to let compounders do their thing, and I’ll sometimes watch a stock for years before ever taking a position.

But that’s exactly why I do this series. It forces me to zoom out, reassess the landscape, and see where sentiment, fundamentals, or valuation have shifted enough to warrant a second look.

Some of these names may quietly disappear from future updates. Others might earn a full deep dive—and maybe, eventually, a spot in the portfolio.

Here are three companies I’m watching as we head into July—and why each one stands out.

JD.com ($JD) – The Undervalued Giant in China Tech

Let’s start with one I’ve followed closely for years. JD has never made it into my portfolio, but with a large portion of my capital exposed to China, I’ve spent plenty of time studying this name—and wrote a deeper dive on it earlier this year (link below).

Few large-cap stocks have fallen as dramatically—or as quietly—as JD. Since its 2021 peak, shares have plunged roughly 68%, pricing in significant deterioration in sentiment and growth expectations.

Yet the underlying business hasn’t crumbled. JD remains one of China’s most crucial e-commerce platforms—vertically integrated, logistics-focused, and profitable.

The company owns warehouses, manages last-mile delivery, and serves hundreds of millions of active users across both discretionary and essential goods.

JD’s heavy investment in logistics infrastructure gives it a unique competitive advantage over rivals, particularly in reliable and fast delivery services, which continue to attract loyal consumers.

What's changed isn't the company—it’s the valuation.

JD now trades at just 8.4x forward earnings and 4.2x EBITDA, significantly below historical averages of 24.5x earnings and nearly 16x EBITDA. At these prices, you're effectively paying a discount for a profitable, cash-generating infrastructure powerhouse deeply embedded in China's digital economy.

JD has also been consistently returning capital to shareholders through meaningful share repurchases, reducing its shares outstanding by approximately 6% over the past year and offering a shareholder yield of roughly 6.2%.

This disciplined capital allocation strategy further underscores JD’s commitment to shareholder value.

The Risks:

The macro backdrop in China remains shaky, consumer sentiment is weak, and aggressive price wars (particularly with Meituan and Alibaba in instant delivery) could pressure margins. Regulatory uncertainty in China also presents ongoing risks.

Still, JD’s integrated logistics, scale, disciplined cost controls, and strategic expansion into underserved markets offer significant long-term resilience.

Topgolf Callaway ($MODG) – Leisure at a Discount

MODG remains one of the more misunderstood consumer stocks out there.

Investors are still struggling to categorize the combined entity that emerged after Callaway's bold move to merge with Topgolf. It's no longer just about selling golf clubs and gear—this is now a hybrid business with a substantial experiential component that drives more than half of its revenue from the fast-growing Topgolf brand.

Yet, sentiment around the stock has soured dramatically. MODG shares are down roughly 65% from their 2023 highs, reflecting both investor confusion and broader consumer spending fears.

Despite the negative sentiment, there's evidence the fundamentals are quietly stabilizing beneath the surface.

Topgolf continues to see improving foot traffic, higher spend per visit, and steadily strengthening unit-level economics. Meanwhile, Callaway's traditional golf-equipment segment remains solidly profitable, generating reliable cash flow and providing financial stability for the combined business.

Valuation, however, is what's especially compelling. MODG trades at only 8.4x EV/EBITDA, well below its historical average (~14x) and a fraction of the multiple you'd typically assign to a consumer brand with a differentiated experiential offering.

It’s also trading at just 0.7x book value, implying the market is placing minimal value on the underlying real estate assets and consumer brand equity.

If Topgolf's experiential, millennial-friendly concept continues scaling, there’s meaningful optionality at these valuation levels.

And considering the brand power, real estate exposure, and the secular shift toward experience-driven leisure, MODG could become attractive as the market gains confidence in the hybrid business model.

The Risks:

Execution remains a significant risk. MODG still carries a meaningful debt load from the Topgolf merger, and integrating these two very different business segments hasn't been seamless. Additionally, discretionary leisure spending tends to be highly sensitive to economic cycles, and an extended consumer slowdown could weigh on revenue growth.

Still, the underlying long-term thesis—capitalizing on consumer preference shifts toward interactive, social leisure experiences—remains solidly intact.

Palantir ($PLTR) – Valuation Insanity

To be clear, this is not a bullish watch.

Palantir has built a strong business. Their government contracts are sticky, the commercial segment is gaining traction, and margins have been improving. They've developed real software IP, and their AI positioning—especially around Gotham and Foundry—has captured the attention of investors.

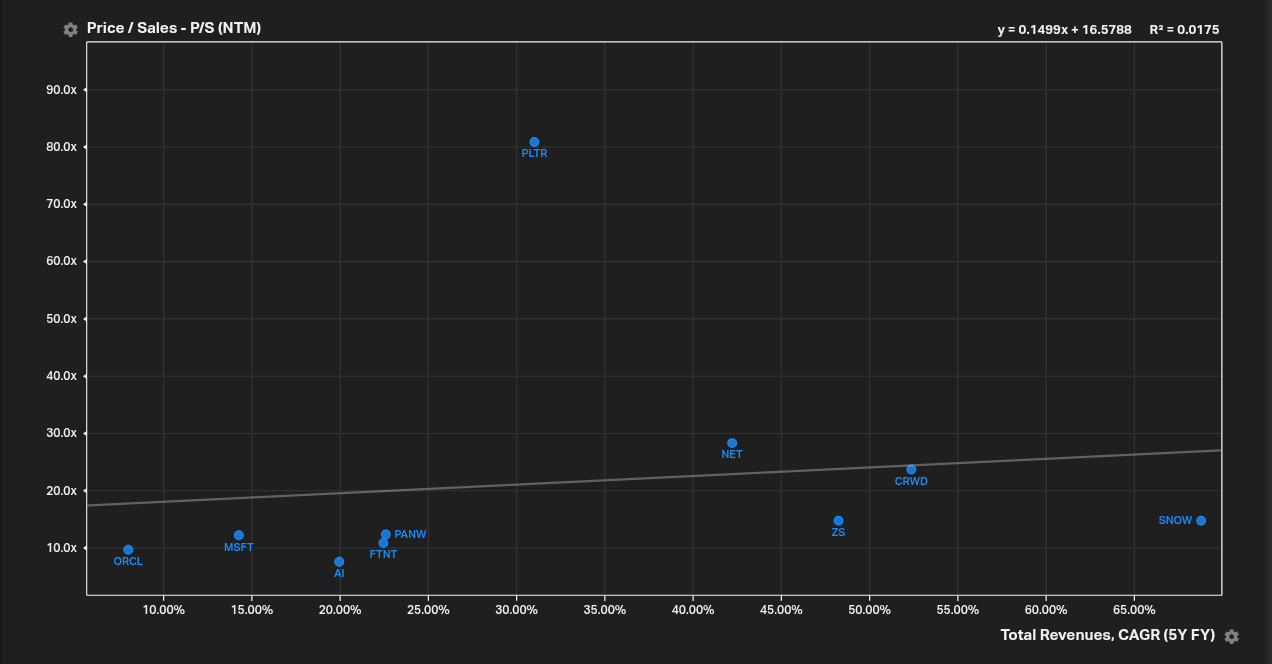

But while the product may be real, the valuation is completely untethered. PLTR trades at 81x forward sales and an absurd 178x forward EBITDA.

It’s not just expensive—it’s in a league of its own.

You can justify high multiples for businesses growing revenue at 50–60% with hyper-efficient operating leverage. Palantir is not that. Growth is solid, not spectacular—25–30% on the commercial side. But overall, the top line remains lumpy and still heavily reliant on government contracts.

The market has priced Palantir as if flawless execution and extraordinary growth are guaranteed for years. Since early 2021, PLTR shares have surged nearly 1400%, dramatically outperforming the broader market.

Even if Palantir executes flawlessly—grows 25% annually, expands margins, and wins more enterprise logos—the math still doesn’t come close to justifying today’s valuation.

There’s no path to growing into 80x sales. That’s not a slight exaggeration—that’s the full story.

Their closest comps—high-growth software and data infrastructure firms like Snowflake, CrowdStrike, or Cloudflare—all trade at lower revenue multiples, despite growing faster and being more operationally scalable. PLTR is the clear outlier.

This isn’t about Palantir missing numbers. It could post strong quarters, guide up, and still fall 40–60% simply because the market decides to re-rate the multiple.

When sentiment turns, multiples matter. And in PLTR’s case, the risk is entirely in the multiple.

Risks (for Bulls):

The company might continue improving operationally, but the current valuation bakes in perfection. Any deviation—slower growth, flat margins, macro hiccups—could be devastating. And even if none of that happens, the stock could still underperform for years just from multiple compression.

This is the definition of a great company, terrible stock—at least at these prices.

The Bottom Line

Three very different setups, each telling a different story about where we are in the market cycle.

JD is a case of deep value in a market that's still out of favor. It’s cheap, unloved, and quietly improving beneath the surface—offering real infrastructure and cash flow at a fraction of its historical multiple.

MODG is a misunderstood consumer play that’s been written off too early. The brand, the footprint, and the real estate are all still there. Now it’s about execution—and the valuation gives you a long runway if they get it right.

PLTR is the opposite. A business that may be executing well but is priced for perfection and beyond. No matter how good the story sounds, the numbers don’t work. Sometimes the biggest risk is the price you pay.

None are obvious buys today, but all three are worth watching. I’ll be looking for dislocations, sentiment shifts, or execution updates that push one closer to portfolio territory.

What stocks are catching your eye lately? Drop a reply—I read them all

Until next time,

Brian

You had me at JD and lost me at PLTR lol … I remember buying JD as a net net might have to put it back on the watch

update here due to locked bur post :

what is u.s. court's leverage vs milei the deadbeat ?

https://english.elpais.com/economy-and-business/2025-07-15/us-court-gives-argentina-three-more-days-to-surrender-its-ypf-shares.html