70% Gross Margins, 25% Growth, Trading at 9x EBITDA

I’ve never been a fan of the “growth at any cost” mindset that dominates today’s market.

Give me a boring, cash-generating machine at 10x earnings over the latest AI darling at 50x revenues any day. But every so often, you come across a company that’s growing at breakneck speed and actually makes money.

Shift4 is one of those rare finds—a high-growth story with real profits to back it up.

Business Overview

At its core, Shift4 is a payment processing company with a unique end-to-end approach that sets it apart from competitors. The company generates revenue primarily through payment processing fees—taking a small cut of every transaction that flows through its system. This creates a beautiful recurring revenue model tied directly to merchant sales volumes.

Unlike pure software players who charge flat subscription fees regardless of merchant performance, Shift4's fortunes rise and fall with their customers' success. This alignment of incentives creates a virtuous cycle: as merchants grow, Shift4 grows. And when economic headwinds hit, the essential nature of payment processing ensures revenue stability even as transaction volumes fluctuate.

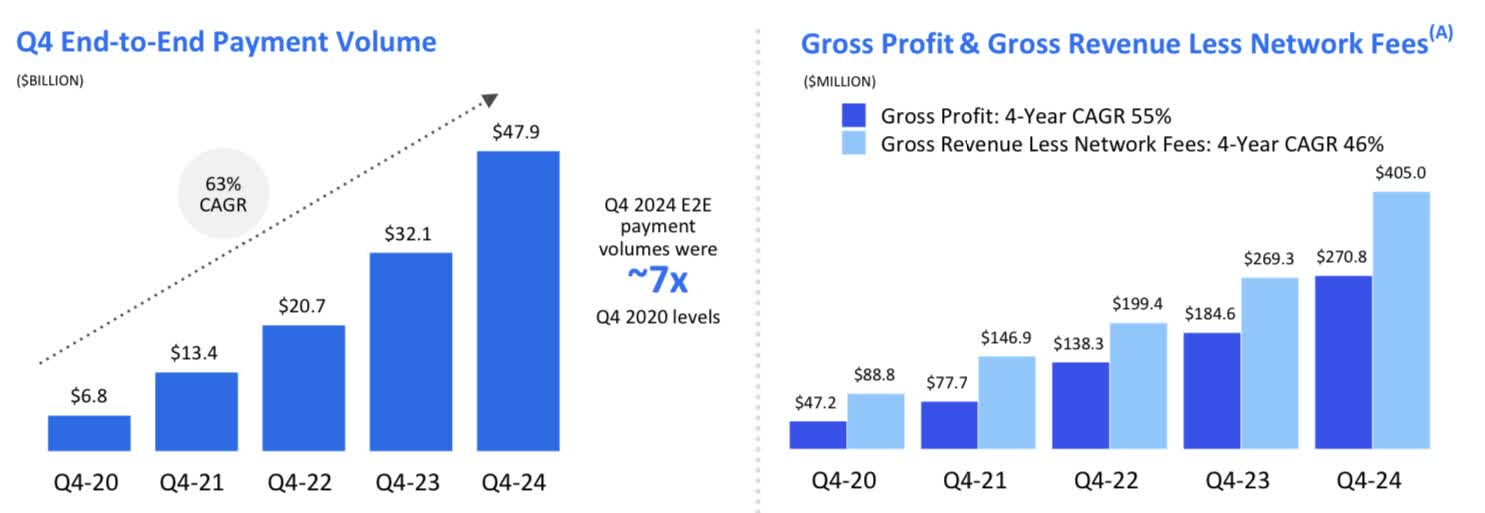

The company operates on impressively fat margins too. Once their payment infrastructure is in place, each additional dollar processed costs almost nothing to handle, leading to gross margins around 70%. This creates substantial operating leverage as volumes scale, with incremental profits flowing straight to the bottom line.

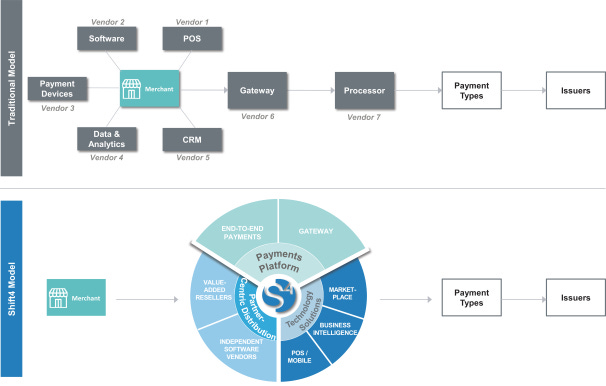

What truly distinguishes Shift4 is their end-to-end payment solution that combines software (point-of-sale systems), hardware (payment terminals), and payment processing into a seamless package. By controlling this entire stack, they can optimize each component while capturing more revenue per merchant relationship than competitors who focus on just one piece of the puzzle.

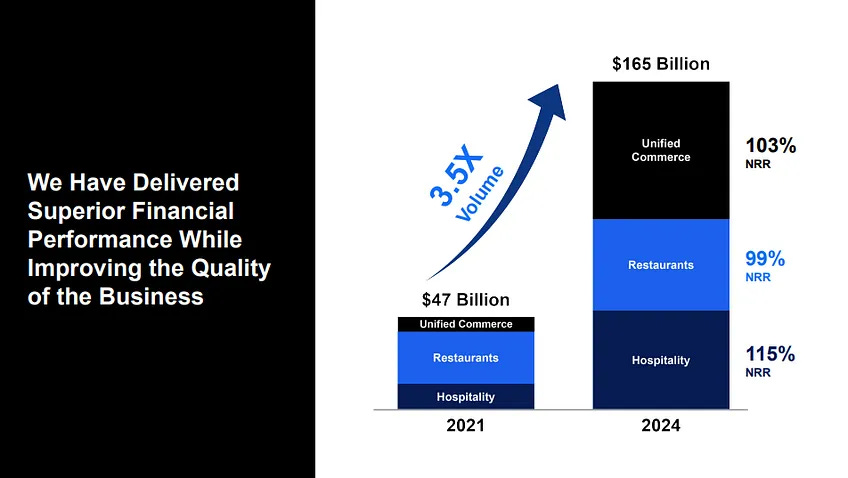

This integrated approach has fueled the company's impressive financial performance: processing $165 billion in payment volume annually while maintaining industry-leading customer retention rates above 90%. And with still less than 5% market share in their core verticals, there's plenty of runway ahead.

Brief History

Founded by Jared Isaacman in his parents' basement back in 1999, Shift4 has grown from a scrappy reseller of POS systems into a payments powerhouse processing hundreds of billions annually. Initially, the company (then called United Bank Card) sustained itself by reselling point-of-sale systems to small bars and restaurants, with a back-end processor handling the actual payment processing on the back end.

Following the 2008 acquisition of HarborTouch, they began offering their own POS software with embedded business management applications, pioneering a model that Square and Toast would later popularize—and get much more credit for.

The real transformation began with the acquisitions of Shift4 (2018) and Merchant Link (2020), payment gateways that carried the company beyond restaurants into hotels and casinos. These gateways serve as middleware between the point-of-sale system and the payment processor, collecting payment information, encrypting it, tokenizing it, and routing it down to legacy merchant acquiring processors.

For years, Shift4 operated primarily in this gateway layer, earning a tiny percentage per transaction while merchant acquirers were skimming 40-100 basis points of transaction value and making significantly more gross profit for easier work. Talk about being on the wrong end of the value chain.

The solution?

Shift4 began claiming the downstream payment processing piece for itself, even waiving gateway fees and subsidizing hardware for clients who dumped incumbent acquirers.

By controlling the entire payments stack, Shift4 was able to capture significantly more economics per transaction while providing clients a more integrated experience. This end-to-end approach became the blueprint as Shift4 expanded into new verticals.

Serial Acquirer

The company's secret sauce—and core to the investment thesis—is a ruthlessly effective playbook of acquiring undermonetized payments assets at reasonable multiples, stripping out costs, and flipping the revenue model from software to payments.

It's like buying rental properties at a discount and immediately raising the rent, except in this case, the tenants actually get a better overall deal.

Keep reading with a 7-day free trial

Subscribe to Coughlin Capital to keep reading this post and get 7 days of free access to the full post archives.