Markel (MKL) — The Perfect Compounder?

I often wonder what separates truly exceptional businesses from those that are just good.

The answer usually comes down to consistency and durability—specifically, whether a company can continue executing its strategy and compounding capital through different economic environments and over decades.

Markel is a prime example.

Since going public in 1986 at $8.33 per share, Markel has quietly transformed that investment into approximately $1,726 today (as of year-end 2024). That's a 207-fold increase, representing a compound annual growth rate of roughly 15% over nearly four decades. For perspective, a $10,000 investment at their IPO would be worth over $2 million today.

Even more impressive, this performance has handily outpaced the S&P 500, which returned about 1,707% over the same period—meaning Markel has delivered more than 8 times the return of the broader market.

Level up your investment research with Koyfin's powerful market analytics platform. I've been using their comprehensive dashboards, real-time data, and intuitive charting tools to make more informed financial decisions. Try Koyfin today using my referral link and get 20% OFF any paid plan.

Try Koyfin Now!

This kind of long-term performance puts Markel among the elite compounders in the financial industry, yet it rarely makes headlines or becomes the topic of debate on social media or in investor circles.

It simply delivers, year after year, for patient shareholders who understand its value.

High-Quality Shareholders, High-Quality Business

One measure of a company's quality is the kind of shareholders it attracts and retains. In Markel's latest annual report, CEO Tom Gayner noted that only Berkshire Hathaway has lower investor turnover than Markel.

This speaks volumes about the trust shareholders place in Markel's long-term approach. The company has built enduring relationships with long-term owners who understand and support their goal of building one of the world's great companies.

"Price is what you pay, value is what you get” — Warren Buffett

With Markel, what you're getting is a diversified financial holding company with three powerful engines working in tandem: insurance, investments, and Markel Ventures (their wholly owned businesses). Each contributes to a system designed for durable, long-term compounding of capital.

Markel approaches business with what Gayner calls the dual time horizons of "forever, and right now." This perfectly captures the balancing act great businesses must perform—making sound daily decisions while building for generations.

As a shareholder, this gives me confidence that short-term quarterly results won't drive foolish long-term decisions.

This philosophy permeates their approach to acquisitions. They only buy businesses they would be comfortable holding forever, applying the same four-part investment principles they use for public securities:

Good return on capital with low debt

Management teams with equal parts talent and integrity

Reinvestment opportunities and/or capital discipline

Reasonable price

These principles have served them well across their three engines of growth and value creation.

1. Insurance: The Foundation Stone

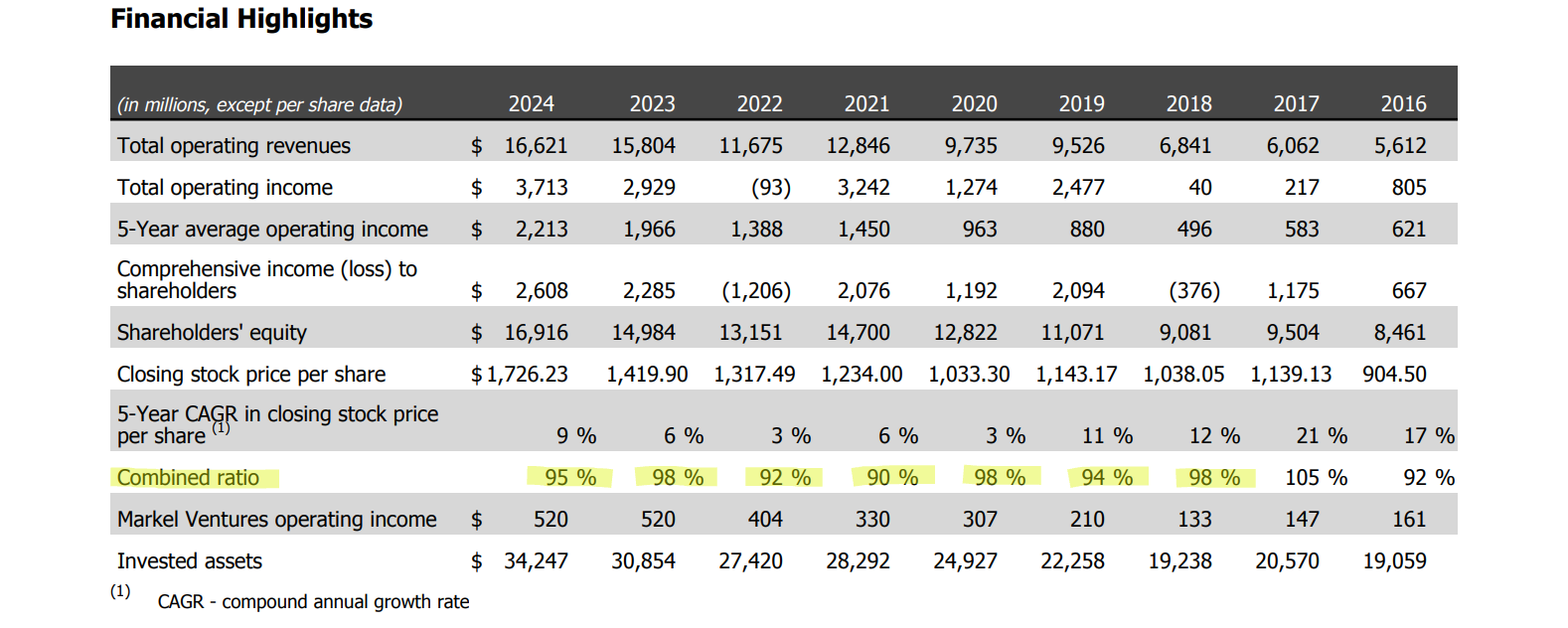

Insurance sits at the core of Markel's business model. In 2024, they posted a combined ratio of 95% (meaning they earned $5 in underwriting profit for every $100 in premium written), improving from 98.4% in 2023.

This marks their seventh consecutive year of underwriting profit—no small feat in the insurance industry.

The company shows discipline by exiting underperforming lines. In 2024, they discontinued various products including intellectual property collateral protection insurance after determining these lines couldn't meet their profitability targets.

As Gayner colorfully put it, they've "had more than a bellyful of selling insurance to sophisticated players looking to do risk arbitrage and financial engineering transactions."

This disciplined approach to capital allocation strengthens the business for the long term.

The international insurance business delivered a sub-80% combined ratio while accounting for about one-third of insurance revenues. That level of outperformance highlights the payoff of Markel’s patience—the international unit, acquired through the Terra Nova purchase in 2000, faced early challenges but has since emerged as a standout under Simon Wilson’s leadership. The Markel International team posted high-single-digit net earned premium growth alongside that impressive combined ratio.

Within the US specialty business, personal lines, property, marine, healthcare, environmental, programs, and commercial professional liability products all produced better-than-target results.

However, challenges remain in construction defects, general liability, and risk-managed professional liability lines—areas the company is actively addressing with portfolio rebalancing and underwriting actions.

2. Investments: The Quiet Accumulator

Markel's investment approach focuses on patiently building positions in high-quality companies and holding them for the long term. In 2024, their equity portfolio returned 20.1%, below the S&P 500's 25% but still contributing to an impressive five-year average annual return of 12.8%.

Many investors overlook the powerful tax advantages of Markel's approach. By holding investments long-term rather than trading frequently, they've built up approximately $2 billion in deferred tax liabilities (on roughly $7.9 billion of unrealized gains). This effectively provides an interest-free loan from the government that compounds over time.

As Gayner explains, "We compounded this interest-free loan steadily and unrelentingly, year by year and decade by decade."

Replicating this low-cost funding would take discipline, constant resistance to short-term pressures, and decades of patience—something most companies lack the temperament to achieve.

Their fixed income portfolio is equally thoughtful, with 98% rated AA or better. These investments aren't just about safety; they're designed to match the duration and currency of insurance liabilities while producing positive spreads.

In 2024, this approach yielded $1.18 billion in "spread," combining $402 million in underwriting profit with $778 million in net interest income.

Markel's invested assets grew to $34.2 billion at year-end 2024, up from $30.9 billion in 2023—an 11% increase.

This portfolio consists of 46% fixed maturity securities, 34% equity securities, and 20% short-term investments and cash equivalents. The composition reflects their balance between safety, liquidity, and long-term growth.

3. Markel Ventures: The Diversification Engine

Markel Ventures, their collection of wholly-owned businesses spanning manufacturing to healthcare, contributes a growing portion of earnings while providing diversification from insurance cycles.

In 2024, Ventures generated $5.12 billion in revenues and $520 million in operating income.

Their Ventures strategy demonstrates patience in acquisitions. They're content to wait on the sidelines when valuations are stretched, as they've noted in recent years. The June 2024 acquisition of Valor Environmental (an erosion control services company) demonstrates their opportunistic approach—they move when they find the right business at the right price.

This discipline extends to how they manage acquired businesses. CEO Gayner describes his role as "CEO of CEOs," focusing on three priorities:

Attracting and retaining talented business leaders

Ensuring those leaders share the Markel Style

Maintaining final say on allocation of discretionary cash flows

The story of AMF Bakery Systems, Markel's first Ventures acquisition in 2005, illustrates their approach perfectly. When acquired, AMF had too much debt despite being well-managed with a strong culture. Under Markel's long-term, low-debt capital approach, AMF thrived even through the inevitable business cycles of equipment manufacturing. Over the past two decades, the business (now Markel Food Group) has grown revenues sixfold and operating income tenfold.

Today, Markel Ventures includes 20 diverse businesses, from Costa Farms (the largest producer of ornamental plants in the U.S.) to Metromont (a manufacturer of precast concrete) to CapTech (a management and IT consulting firm). What binds them together is a commitment to the Markel Style and long-term value creation.

Balance Sheet Strength and Intrinsic Value

The foundation of Markel's long-term compounding is its fortress-like financial position. With a debt-to-capital ratio of just 20% (unchanged from 2023 and deliberately maintained within their target range) Markel embodies the principle that financial strength provides both defense and offense in capital allocation.

Total shareholders' equity reached $16 billion in 2024, up from $15.0 billion at the end of 2023, continuing the relentless march upward that has defined the company since its IPO.

This balance sheet strength directly enhances Markel's intrinsic value in multiple ways. First, it provides optionality—the ability to capitalize on opportunities that arise during market dislocations when others are forced to retrench. Second, it reduces risk, creating a margin of safety against unforeseen challenges. Third, it lowers the cost of capital, improving returns over time.

As Gayner notes in the annual report, "We see our strong capital position and low-debt philosophy as necessary preconditions for long-term thinking."

The most visible manifestation of this value creation is Markel's remarkable book value growth—from a mere $3.42 per share at its 1986 IPO to $1,276.31 by year-end 2024, representing a 16.9% compound annual growth rate over nearly four decades.

Few financial companies in history have maintained such a consistent trajectory of value creation across multiple economic cycles, interest rate environments, and management transitions. Yet despite this proven track record, Markel shares currently trade at approximately $1,771.42 — a price-to-book ratio of about 1.4x.

While this doesn't immediately scream "bargain" to value investors focused solely on traditional metrics, it actually represents a substantial discount to the company's intrinsic value.

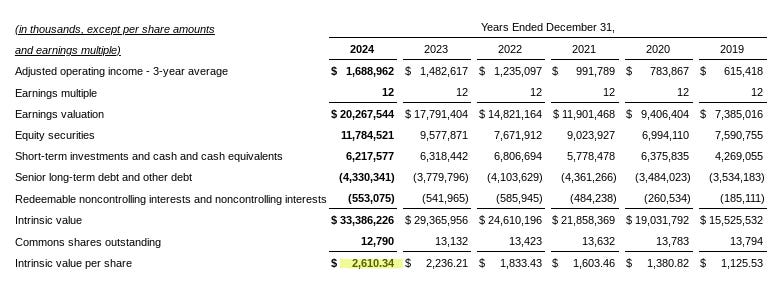

Management's methodology suggests intrinsic value around $2,610 per share as of December 31, 2024—indicating the stock trades at roughly a 32% discount to what the business is actually worth.

More telling still is the five-year compound annual growth rate in intrinsic value of 18%, which has outpaced the growth in stock price over the same period. This widening gap between price and value creates what Buffett might call a "coiled spring" for patient investors—a situation where the market's short-term thinking provides an opportunity for those with a longer horizon.

The method Markel uses to calculate intrinsic value isn't complex financial engineering designed to flatter management.

It simply applies a conservative multiple to a three-year average of adjusted earnings (smoothing out short-term fluctuations) and adds the value of investments and other balance sheet assets. This approach aligns with the company's broader philosophy of transparency and long-term thinking.

In essence, Markel offers an increasingly rare combination in today's market: financial fortress-level safety with meaningful upside potential. The balance sheet provides downside protection, while the discount to intrinsic value offers substantial appreciation opportunity—creating an asymmetric risk-reward profile that value investors like myself dream about.

The Psychology of Owning Markel

There's tremendous value in owning businesses that let you sleep well at night. Markel is such a business. The consistency of their messaging and execution over decades creates trust that's hard to quantify but invaluable to shareholders.

A sign of truly exceptional management is alignment between what they say and what they do. Markel has demonstrated this alignment for decades, building a consistent track record under a succession of leaders who all share the core philosophy established by the Markel family.

"We believe that great companies do things for their customers, colleagues, and shareholders rather than to them." — Tom Gayner

Their “win-win-win” philosophy of creating positive outcomes for customers, employees, and shareholders provides a framework that prevents the short-termism that plagues many public companies.

As the late Charlie Munger said, "The big secret in life is that there is no big secret. Whatever your goal, you can get there if you're willing to work."

Markel exemplifies this patient, methodical approach to building value.

They don't promise overnight riches or dazzle with complicated financial engineering. Instead, they focus on the fundamentals: disciplined underwriting, thoughtful investing, and adding quality businesses to their portfolio when opportunities arise.

The company's 38-year track record of growing book value per share at approximately 16.9% annually and stock price at about 15% annually places it among the elite compounders in the financial industry. Few companies can match this level of consistent value creation over such a long period.

For long-term investors looking for a well-managed business that compounds capital at attractive rates through various economic environments, Markel stands out as an excellent choice. The fact that company insiders and long-term shareholders rarely sell their shares tells you everything you need to know.

In a market often dominated by short-term thinking, holding Markel for the long haul makes sense.

After all, the real money isn't made in the buying or selling–it's in the waiting. Or as CEO Tom Gayner might put it, drawing on Markel's redwood tree analogy, it's about being part of something that's built to endure for centuries, not just quarters.

Redwood trees—and great companies—aren't made in a day, but their longevity and majesty make them worth the wait.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Please conduct your own research and consult with a financial advisor before making any investment decisions.

Great summary of great business. As was last post on NNI. Probably worth a paid scrip!