A Timeless Brand at 3.7x FCF, Repurchasing 30% of MC

An iconic American brand with dominant market share in core segments.

I was screening for value stocks this weekend when a surprising name caught my attention.

Harley-Davidson (HOG), the iconic American motorcycle manufacturer, trading at just 3.7x P/FCF and 7.6x TTM earnings. The symbol of freedom and American road culture available at bargain-basement prices? I needed to investigate further.

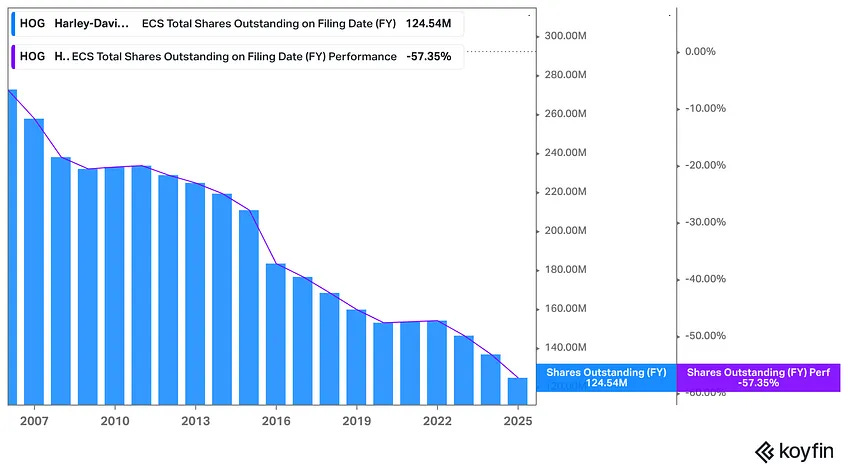

The thing that really grabbed my attention was their buyback history. Harley has reduced its outstanding shares by a staggering ~57% over the last two decades.

That's not a typo. The company has more than halved its share count over 20 years, bringing it down to just 124.54 million shares. In 2024 alone, they repurchased $450 million worth of stock (12.5 million shares). For context, their current market cap is approximately $3.2 billion.

Level up your investment research with Koyfin's powerful market analytics platform. I've been using their comprehensive dashboards, real-time data, and intuitive charting tools to make more informed financial decisions. Try Koyfin today using my referral link and get 20% OFF any paid plan.

Try Koyfin Now!

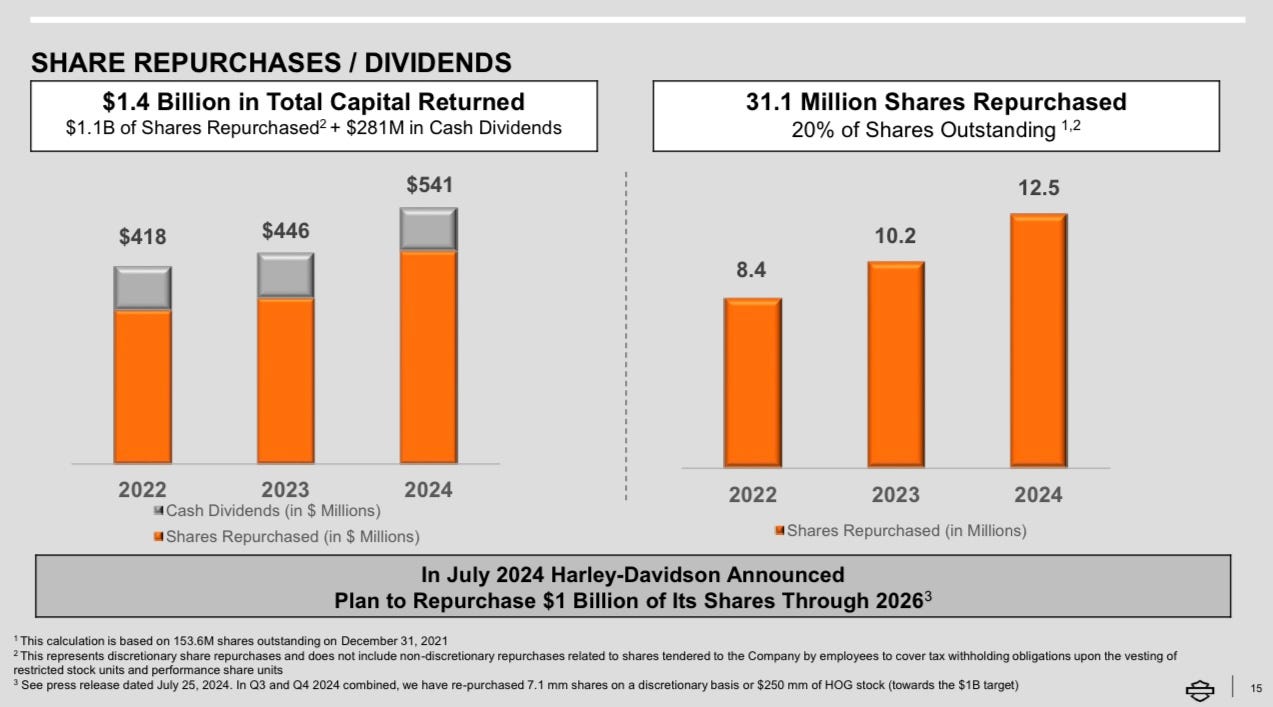

Last July, Harley announced plans to repurchase an additional $1 billion of shares through 2026, which at current prices represents roughly ~30% of the entire company. This comes on top of the $1.4 billion they've already returned to shareholders since 2022 through buybacks and dividends.

The buyback story undoubtedly looks impressive at first glance:

57.35% reduction in shares since 2006

$450 million repurchased in 2024 alone ($250 million in H2)

$1 billion buyback plan announced through 2026

As of Q4 2024, they've repurchased 7.1 million shares toward that $1 billion target

But here's where the narrative takes a concerning turn.

Harley's share repurchase timing has been problematic at best. They've consistently bought at high prices (often $40-50 per share) while the stock now sits at $26. This isn't hindsight bias—it's fundamental capital allocation failure. When management buys back shares at inflated prices, they destroy shareholder value rather than create it.

In practical terms: If Harley spent $100 million buying back stock at $50, they retired 2 million shares. Had they waited and deployed that same capital at today's $26, they could have retired 3.85 million shares—nearly twice as many.

Multiply this across billions in buybacks, and you've identified a serious problem.

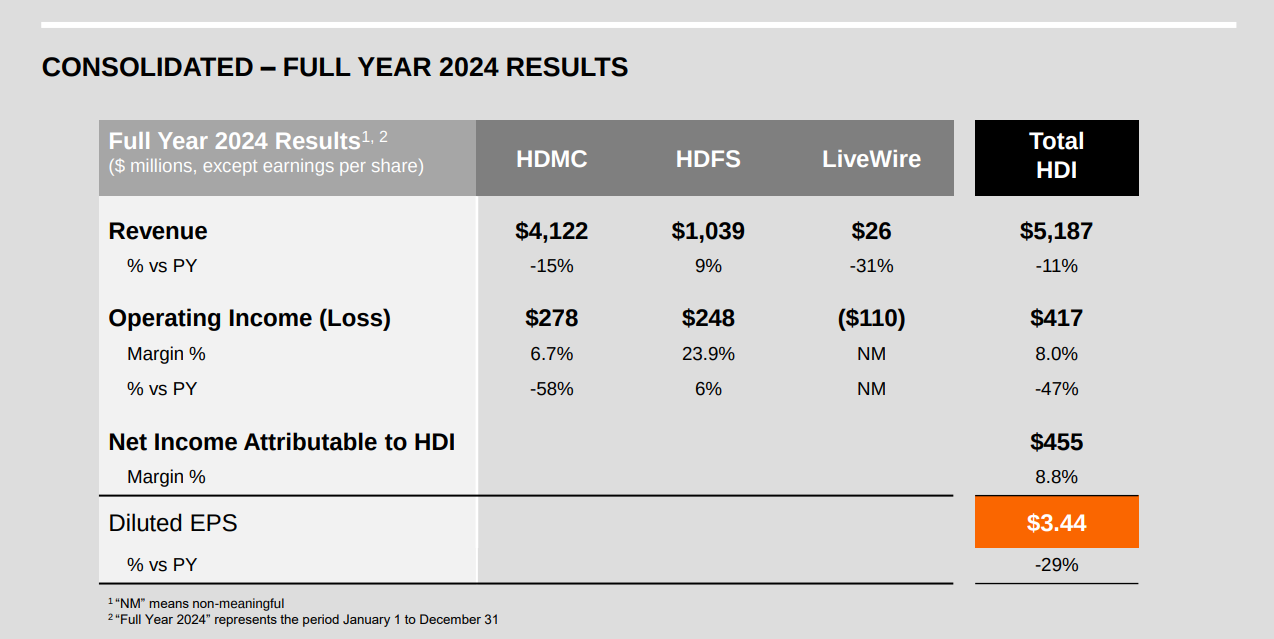

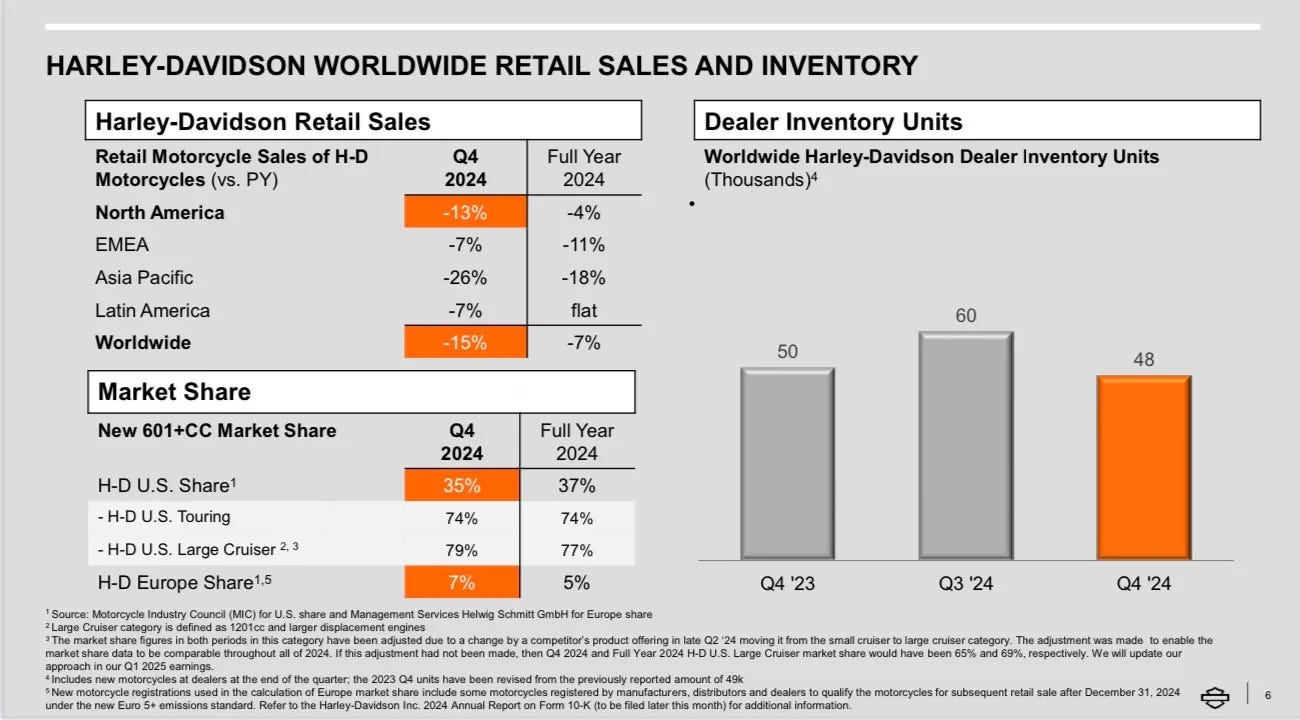

HOG FY24 Results:

Revenue down 11% to $5.19 billion in 2024

Net income collapsed 36% to $455 million

EPS dropped 29% to $3.44

Operating margin at HDMC (motorcycle segment) halved from 13.6% to 6.7%

Global motorcycle shipments declined 17% to 148,862 units

Yet despite these warning signals, the buybacks continue unabated—like watching someone bail water from a leaking boat instead of repairing the hole.

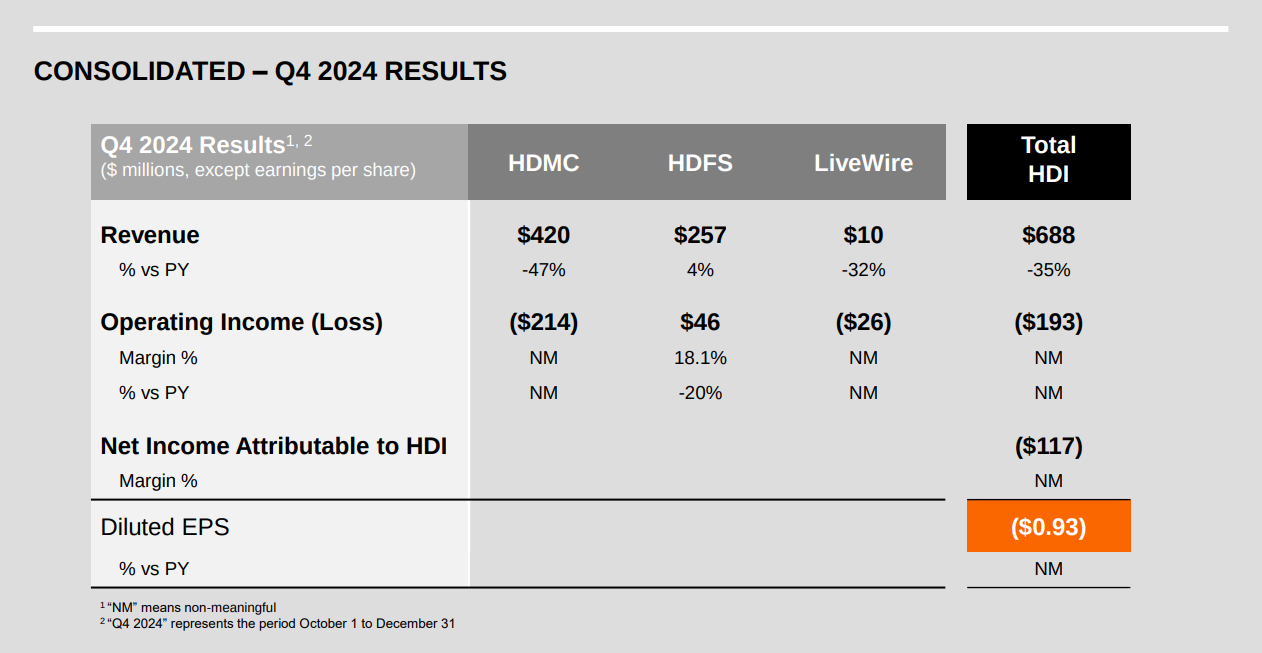

The Q4 results look even worse, with consolidated revenue down 35% year-over-year and an operating loss of $193 million. This wasn't just a small seasonal dip; it was a substantial deterioration in performance that should raise red flags for any investor.

The demographic challenge clearly remains persistent and real. Harley's core customers are aging, while younger riders gravitate toward cheaper, sportier alternatives.

Despite efforts to attract millennials through LiveWire (their electric division) and adventure touring models, premium pricing remains a significant barrier to entry. The LiveWire division itself continues to struggle, with a 31% revenue decline in 2024 and only 612 units sold—hardly the growth engine Harley positioned it to be.

Then there's the debt situation: $7 billion outstanding against $1.6 billion in cash.

That's a debt-to-equity ratio of 1.57x—not catastrophic, but certainly concerning when sales are declining and the Harley-Davidson Financial Services segment is experiencing rising credit losses (3.3% in 2024, up from 3.0% in 2023 and 1.9% in 2022). This deteriorating credit quality suggests their financing arm may become a liability rather than a profit center if economic conditions worsen.

Is there anything to be optimistic about? Sure (maybe lol).

If you've persevered through the concerns, here's where the story gets a little more intriguing. Beneath the troubling financials lies a surprisingly compelling story line that shouldn't be ignored.

1. Dominant Market Position

Despite years of challenges, Harley maintains an enviable market dominance that competitors can only dream of:

74.5% market share in the U.S. Touring segment

77% share in the U.S. Large Cruiser category

65% share in the U.S. electric road bike market through LiveWire

This overwhelming market leadership isn't just a vanity metric—it represents tremendous pricing power and brand equity that few consumer companies can match.

2. Premium Strategy That's Actually Working

Contrary to what declining unit sales might suggest, Harley's premiumization strategy has delivered impressive results.

The company has increased per-unit profitability by a remarkable 185% since 2019, transforming their business model from volume-dependent to margin-focused.

This "fewer but better" approach aligns perfectly with luxury brand positioning. After all, Ferrari sells far fewer vehicles than Toyota, but nobody questions their business model. Selling fewer bikes at higher margins creates exclusivity that reinforces the brand's premium status—when executed correctly.

3. Leadership with a Proven Turnaround Playbook

Harley isn't adrift without direction. CEO Jochen Zeitz is executing a five-year strategic plan called "The Hardwire" that addresses the company's core challenges head-on.

Zeitz isn't just any executive—he previously orchestrated Puma's remarkable transformation from a struggling brand to legitimate challenger to Nike and Adidas. His approach wasn't merely product-focused; it centered on repositioning Puma as a lifestyle brand representing individuality and self-expression.

Sound familiar? That's precisely the transformation Harley-Davidson needs.

The Hardwire plan has several promising pillars:

Focus on strength: Doubling down on the most profitable segments (Touring, large Cruiser, Trike)

Margin expansion: Targeting 15% operating margins (they achieved 13.6% in 2023 before 2024's setback)

Future-proofing: Electric motorcycle expansion through LiveWire

Demographic balance: Attracting younger riders while preserving heritage

Operational excellence: $400 million in cost productivity targeted by 2025

Early results showed promise, with cost savings of $135 million and significant margin expansion in 2022-2023. The 2024 setback raises questions about sustainability, but the blueprint for success exists.

4. LiveWire: Future Growth Engine?

The LiveWire electric motorcycle division presents both opportunity and risk. While it continues to generate substantial operating losses ($110 million in 2024), management projects a 40% reduction in cash burn for 2025—a significant improvement if achieved.

Rather than seeing LiveWire as just a money pit, consider it a strategic hedge against industry disruption. Electric vehicles are transforming the automotive landscape, and Harley is positioning itself to be relevant regardless of how powertrain technologies evolve.

The real question isn't whether LiveWire is profitable today (it's not), but whether it gives Harley optionality in a rapidly changing market. If electric motorcycles gain mainstream adoption, Harley will be miles ahead of traditional competitors still figuring out battery technology.

5. Aggressive Buybacks Could Supercharge Returns

While the timing of Harley's past share repurchases deserves criticism, their current buyback program could prove incredibly bullish if the business stabilizes. With shares trading at just 7.6x earnings, each dollar spent on buybacks creates significantly more value than when the stock was at $40-50.

As I mentioned earlier, the announced $1 billion repurchase program through 2026 represents approximately ~30% of the current market cap. If Harley simply maintains its earnings power—let alone grows it—the reduction in share count will substantially increase EPS and potentially drive the stock higher.

As long as the company manages its debt burden prudently and generates sufficient free cash flow, these buybacks represent a compelling use of capital at current valuations. Even modest operational improvements could combine with the reduced share count to deliver outsized shareholder returns.

The Bottom Line

Harley-Davidson is a classic case of conflicting signals. On one hand, the valuation metrics are screaming "buy!" louder than a Harley roaring down Main Street. But on the other hand, the company's deteriorating operational metrics suggest proceeding with caution.

So what gives? Why the massive discount?

Well, for starters, management's aggressive share buybacks at elevated prices destroyed a boatload of shareholder value. Instead of saddling up more debt to repurchase stock, Harley would've been better served investing that cash into new product development or paying down existing liabilities.

Sure, retiring half your shares might sound impressive, but if you overpay, it's all just smoke and mirrors.

Yet despite these missteps, I believe Harley still has a few key ingredients that could fuel a potential turnaround:

An iconic brand that's recognized from Milwaukee to Mumbai

Dominant market share in core segments

Strong cash generation ($1B+ last year)

A CEO with legit turnaround chops

At current valuations, Harley shares offer an intriguing asymmetric bet. If the new leadership team can simply stabilize the business the stock could see a major multiple expansion.

For now, I'm watching this one from the sidelines. The shrunken share count does provide a meaningful tailwind if they can kickstart growth in the core business again. But if bike sales keep declining and margins erode further, not even the mother of all buybacks will keep this stock running.

As the old investing adage goes: "Don't try to catch a falling knife." Harley-Davidson might be exactly that—a "cheap" stock that keeps getting cheaper.

Personally, I'd rather wait for more evidence that management's turnaround plan is gaining traction before hitting the throttle on HOG shares. Fortune may favor the bold, but it rarely rewards the reckless.

I agree it is an interesting idea. To me HOG is an iconic brand, but perhaps changing customer tastes of the younger generation outweighs this. They seem to want to ride e-bikes and e-scooters, not Harleys. Financial performance has been poor for a long time. ROIC at 6% on average since 2009. Operating profit and the stock price peaked in 2006! I don't know the history of the company well enough, I wonder how many management teams have presented turnaround plans over the past 15 years.

Great piece, thanks for sharing. So HOG dominates a premium segment but with a ‘structural headwind’ - margin compression and decline in demand, so where does the CEO think the opportunity lies?