Adyen (ADYEY) — Still Scaling, Still Underowned

A deep dive into Adyen’s business model, margins, growth, and why the stock remains underappreciated despite scale.

“At Adyen, everything we do is engineered for ambition. We started with payments, at a time when providers offered services based on a patchwork of systems built on outdated infrastructure. Ambition demanded more. So we set off to build a financial technology platform for the modern era, entirely in-house, from the ground up."

Adyen processed over €1.29 trillion in payments last year. That kind of scale would usually come with a ton of noise, but Adyen has done it quietly. No big marketing campaigns, no flashy brand, no hype machine. Just execution.

That’s part of what makes the story so compelling. This is one of the most disciplined fintech operators in the world—focused entirely on building infrastructure for enterprise-grade payments. It’s not trying to be everything to everyone. It’s not chasing SMBs or launching consumer wallets. It just builds tools that help some of the world’s biggest companies move money more efficiently.

The stock has never looked cheap on traditional metrics, and probably never will. But for long-term investors, that might be missing the point.

Adyen’s business is built to scale. With a unified global platform, best-in-class margins, and virtually zero churn among large clients, it’s a machine that compounds quietly in the background. And despite the bump in 2023 from over-hiring, the operating model is back on track, with margins and free cash flow pushing toward all-time highs.

This is a company that can grow earnings 20%+ annually for a long time, generate elite-level returns on capital, and do it without playing the typical fintech growth games. There just aren’t many businesses out there that look like this—high growth, high margin, and built on real infrastructure.

The thesis is straightforward: Adyen is one of the few high-growth fintechs with true infrastructure economics—recurring volume, high switching costs, and operating leverage that gets stronger with scale. The market overreacted to short-term margin compression, but the fundamentals never broke. With normalized hiring, margins are climbing again, and FCF conversion remains best-in-class.

Company History

Adyen was founded in 2006 by Pieter van der Does and Arnout Schuijff, two former executives at Bibit, a Dutch payments company acquired by the Royal Bank of Scotland in 2004. Their time at Bibit gave them a front-row seat to the dysfunction of the legacy payments ecosystem. Global merchants were forced to cobble together gateways, processors, risk tools, and acquirers just to accept payments across markets. Approval rates were inconsistent. Settlement timelines were slow. Reporting was fragmented. Fraud tools didn’t talk to reconciliation systems. The stack wasn’t just clunky—it was broken.

“The idea was never to build another layer. It was to start from scratch and get rid of the inefficiencies in global payments.” — Pieter van der Does

They didn’t want to bolt on another piece. They wanted to rebuild it entirely. Hence the name "Adyen," which means "start again" in Sranan Tongo (a creole language spoken in Suriname). The company’s founding vision was to offer a single, unified platform that handled every step of the payment journey: checkout, fraud screening, acquiring, processing, settlement, and reporting. All of it built from scratch, all on one codebase, and deployed globally.

The early pitch resonated with a very specific customer base: fast-scaling digital-first platforms. Spotify, Uber, Facebook, and Dropbox were among the first wave of adopters—businesses that needed to operate in dozens of countries without managing dozens of integrations. Adyen’s global reach, clean APIs, and high authorization rates made it the obvious pick. By 2012, it landed eBay as a client, replacing PayPal as the marketplace's primary payment processor. That marked a turning point. From there, the company became the default infrastructure choice for large-scale, cross-border commerce.

Adyen reached profitability early and never deviated from its focus. It raised relatively little capital—just over $260 million in total, with its last primary round in 2015—and went public in 2018 via a direct listing on the Euronext Amsterdam. No new capital was raised in the IPO.

Equally important is what Adyen didn’t do. It never launched a consumer wallet. It didn’t enter the small business market. It never tried to expand via acquisition. And it never diluted its culture chasing growth. The company remained relentlessly focused on building enterprise-grade infrastructure for global merchants, with disciplined hiring, product-first leadership, and a long-term orientation.

Nearly two decades in, that original blueprint still defines how Adyen operates today. And the fact that it reached over €1.2 trillion in processed volume last year—with no debt, minimal dilution, and very little marketing—makes it one of the most quietly impressive fintech stories of the last generation.

Business Overview

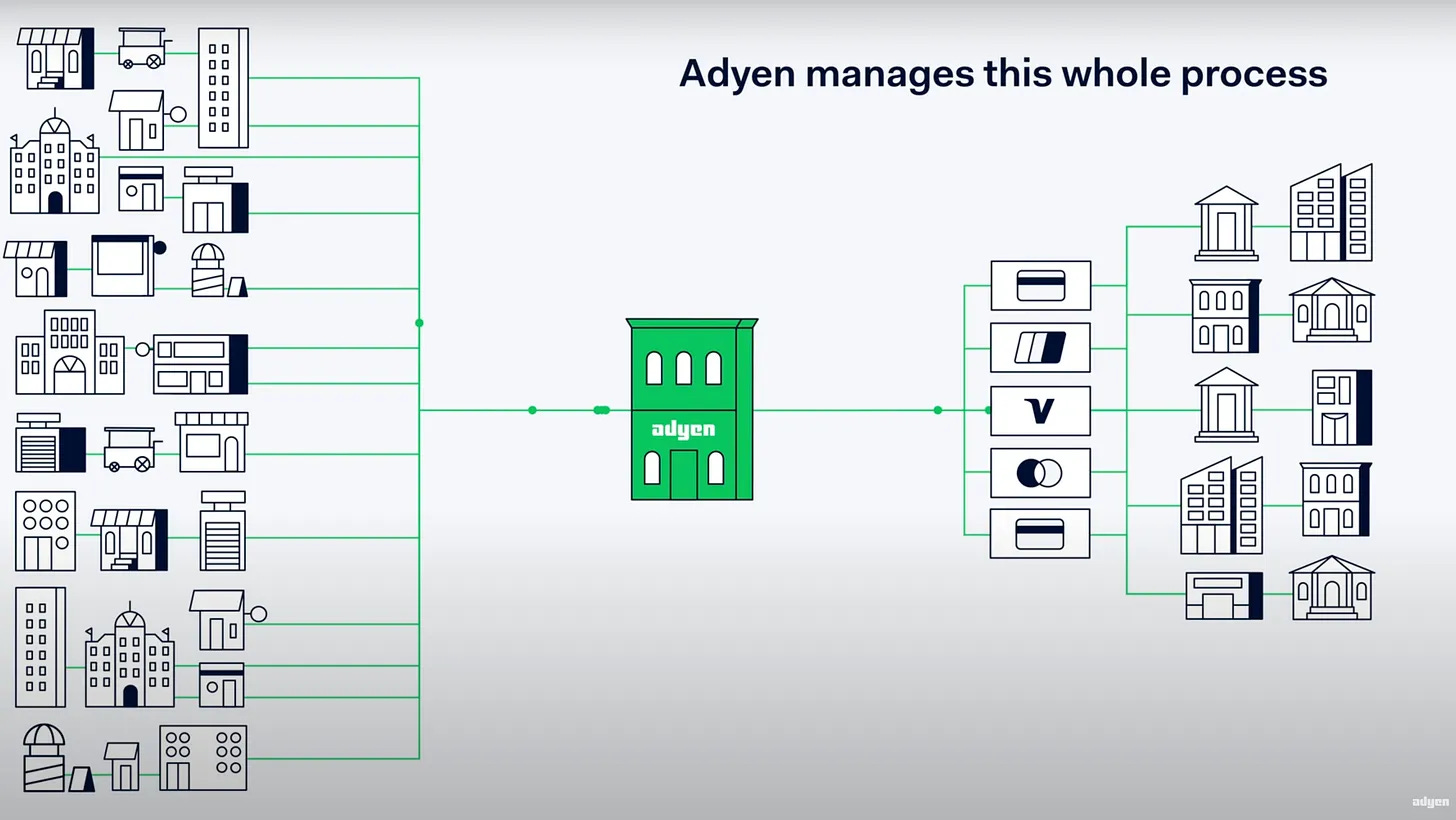

Adyen sits deep in the global commerce stack, powering payments for some of the largest and most complex merchants in the world. It doesn’t offer a single product. It offers an integrated platform that spans every stage of the payment lifecycle—from checkout to risk, acquiring, settlement, and reconciliation.

The business is deceptively simple in how it presents itself, but under the hood it’s an intricate infrastructure machine.

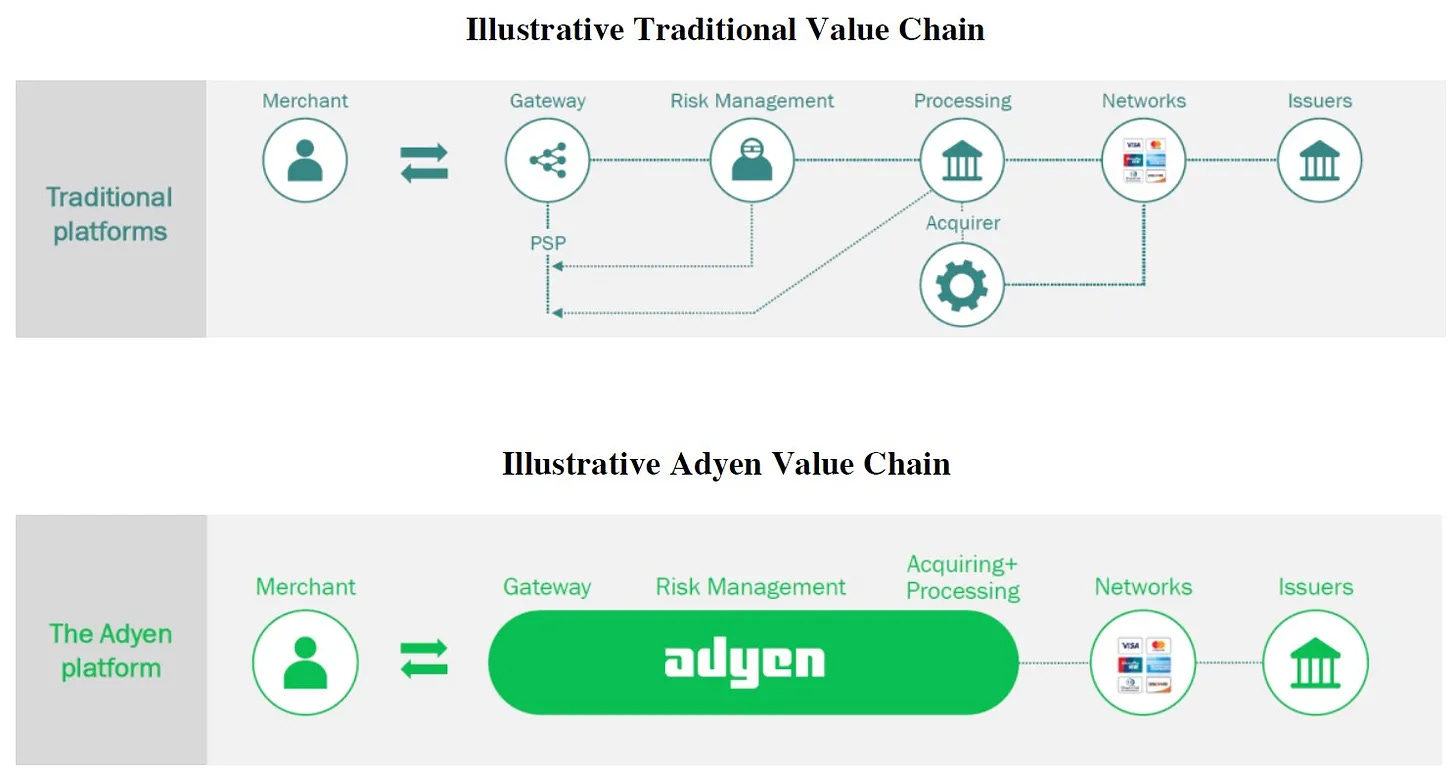

Most legacy setups require merchants to stitch together multiple vendors: a front-end checkout system, a fraud detection tool, a third-party acquirer, and a reconciliation engine on the backend. Adyen replaces that sprawl with a vertically integrated stack: one API, one contract, one dashboard.

Adyen controls the full value chain. It acts as the gateway, the risk engine, the processor, the acquirer, and the settlement layer. Crucially, it holds acquiring licenses in major global markets—including the U.S., EU, UK, Brazil, Singapore, Australia, and more—which gives it direct access to local card networks and banks. That setup improves reliability, reduces latency, and allows for richer transaction data.

The result is not just smoother operations—it’s a real margin advantage. With fewer intermediaries, Adyen can offer better pricing and approval rates while capturing more economics per transaction. The in-house architecture also feeds data back into its fraud tools and reporting dashboards, driving smarter decision-making and higher conversion.

Because the stack is built natively the platform behaves consistently across geographies. Whether a merchant is accepting QR codes in Singapore or Visa debit in Canada, it’s all processed through the same system. That reduces technical complexity and gives global merchants a single point of accountability. For enterprise clients with omnichannel operations, that consistency is a major selling point.

Adyen’s customer base is concentrated at the high end of the market. Spotify, Microsoft, Uber, eBay, Etsy, Booking.com, H&M—these are global-scale businesses running high-volume, cross-border flows. What they need isn’t just a payment processor. They need infrastructure that delivers performance: higher approval rates, lower fraud, faster reconciliation, and granular data.

The company supports both online and in-person transactions. On the in-store side, Adyen offers its own payment terminals—but not as a hardware play. The terminals are simply a physical extension of the core platform, offering unified reporting and settlement across all channels. That makes Adyen especially compelling for large omnichannel retailers.

Another major growth area is Adyen for Platforms—its embedded finance offering for marketplaces and software platforms. This business powers the financial backend for players like Etsy and GoFundMe, handling onboarding, compliance (KYC), payouts, issuing, and treasury services behind the scenes. It’s an infrastructure layer that lets platforms embed payments—and increasingly financial services—natively into their product.

Revenue is generated primarily through net transaction fees—a small markup (typically 14–16 basis points) on top of interchange and scheme fees. While the take rate may seem low, the model scales beautifully. Once a merchant is integrated, incremental volume costs very little to process. That operating leverage drives high gross margins and makes scale a key moat.

Level up your investment research with Koyfin's powerful market analytics platform. I've been using their comprehensive dashboards, real-time data, and intuitive charting tools to make more informed financial decisions. Try Koyfin today using my referral link and get 20% OFF any paid plan.

Adyen doesn’t rely on aggressive sales tactics to grow. Sales and marketing spend remains below 5% of revenue. The product tends to sell itself—through performance, reputation, and word of mouth. Once a merchant is onboarded, expansion tends to follow naturally: new geographies, new payment methods, and deeper integration over time.

This is a company that doesn’t need to constantly reinvent itself. The platform was built with scale in mind, and it’s compounding efficiently as global digital commerce continues to grow. As long as Adyen keeps executing, the business model should do the rest.

Industry & Competitive Landscape

Payments is a fiercely competitive space—and one that’s only grown more crowded over the last decade. On paper, it looks like a commoditized business: hundreds of providers moving money from point A to point B, with little to differentiate them. But in practice, the differences between vendors are vast. And Adyen has carved out a particularly durable corner of the market.

Keep reading with a 7-day free trial

Subscribe to Coughlin Capital to keep reading this post and get 7 days of free access to the full post archives.