(BABA) Alibaba Update — Q3/FY2024

Alibaba Group (BABA) just announced its results for Q3 FY2024 (the quarter ended December 31, 2024), and the numbers paint a picture of renewed acceleration across many core business segments. For shareholders who have been patiently waiting for the company’s fundamentals to improve, this quarter suggests that “the old Alibaba” may be on its way back.

Given my large allocation to Alibaba (my largest single-stock position) I’m obviously watching developments closely. Additionally, I maintain a broader bullish stance on other Chinese equities. I believe that China’s shift toward a more pro-business, pro-consumption environment bodes well for companies like Alibaba, which sit squarely in the center of both domestic and cross-border commerce.

In this post, I will share my detailed review of the quarter’s financials, discuss the most important takeaways for investors, and explain why I remain bullish on Alibaba.

(If you haven’t already, check out my full Alibaba Investment Thesis below)

1. Recap of Key Numbers

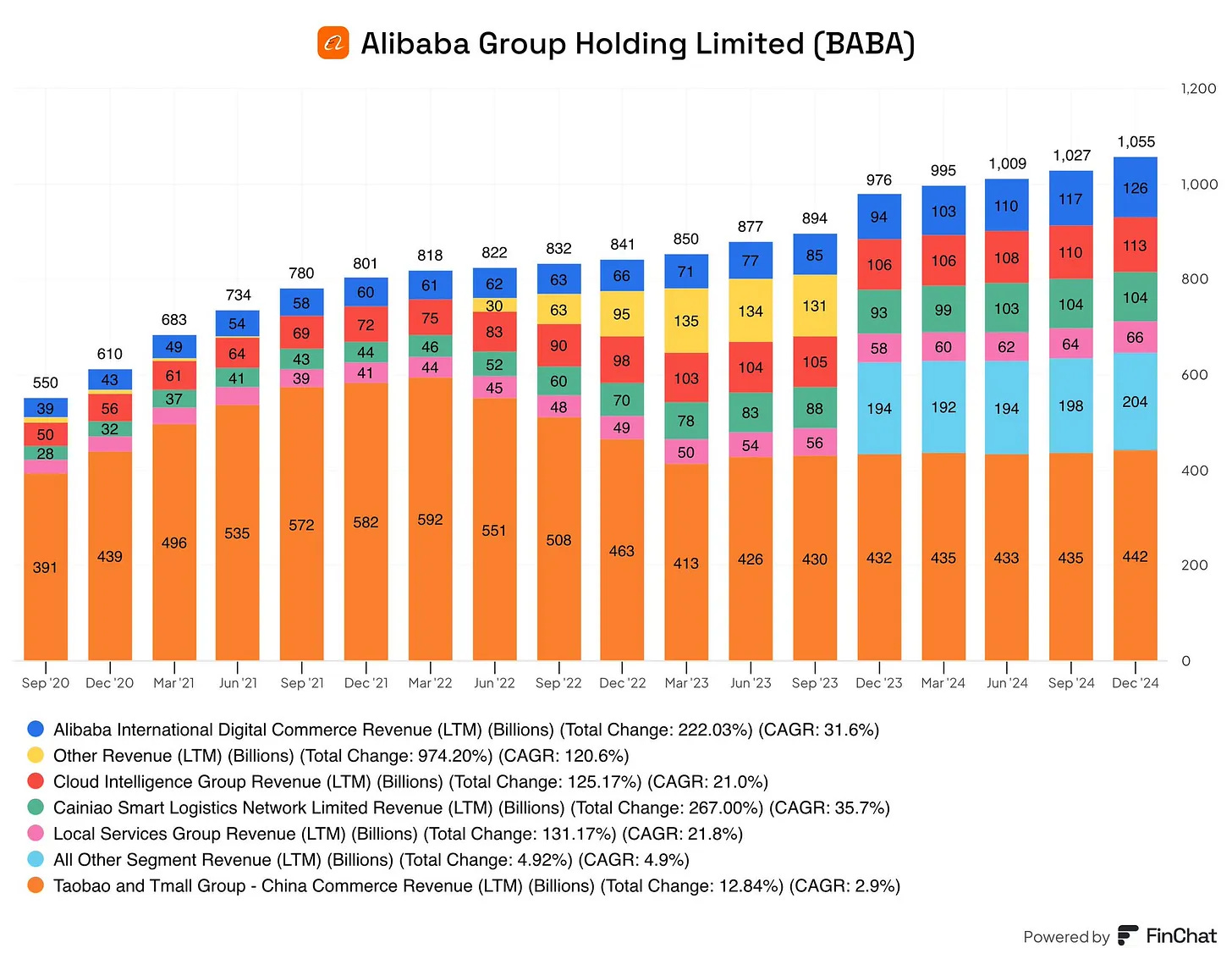

Total Revenue:

RMB280.15 billion (US$38.38 billion), up 8% year-over-year.

This represents an improvement from the 5% year-over-year uptick in the prior quarter, highlighting an accelerating top line.

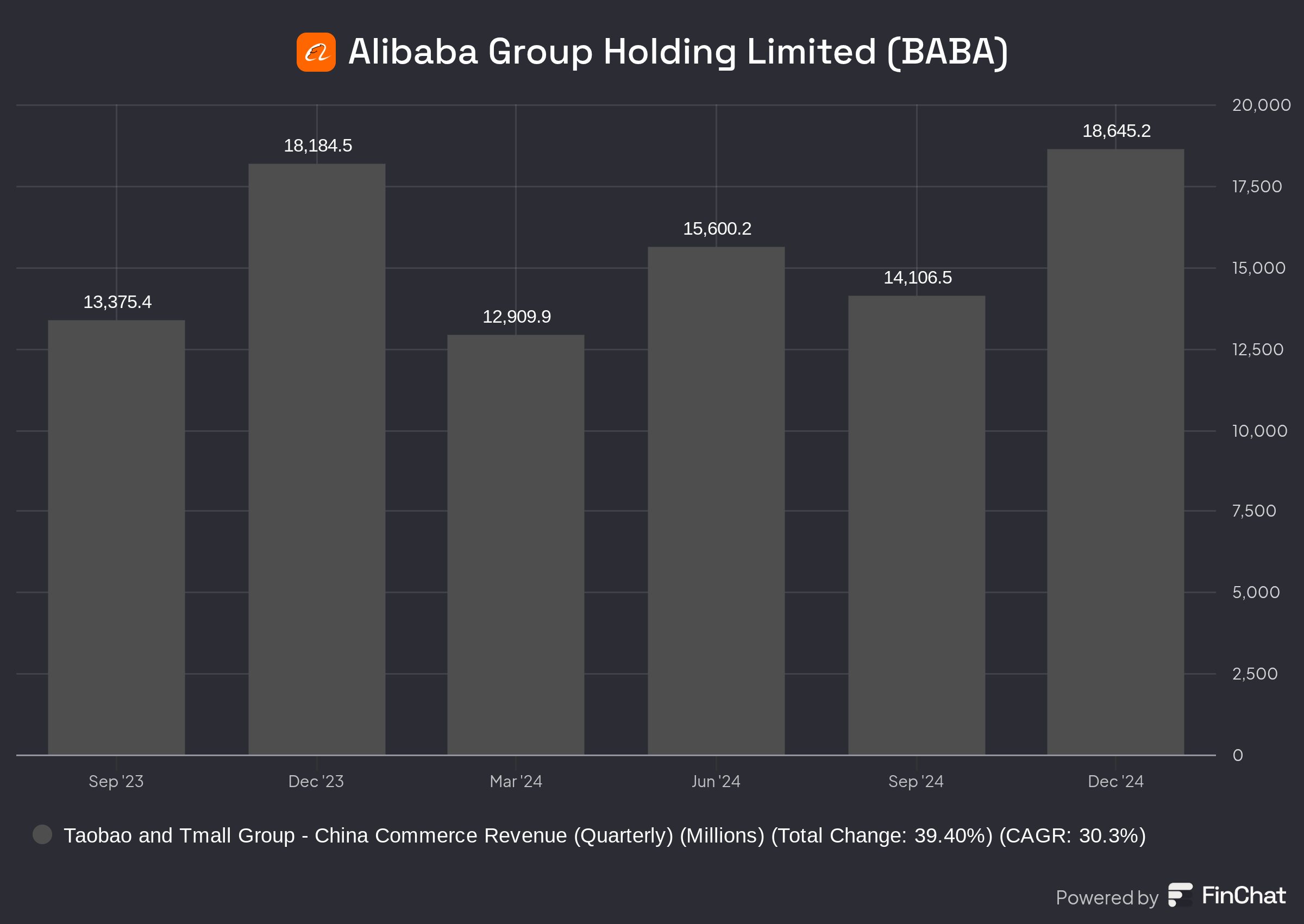

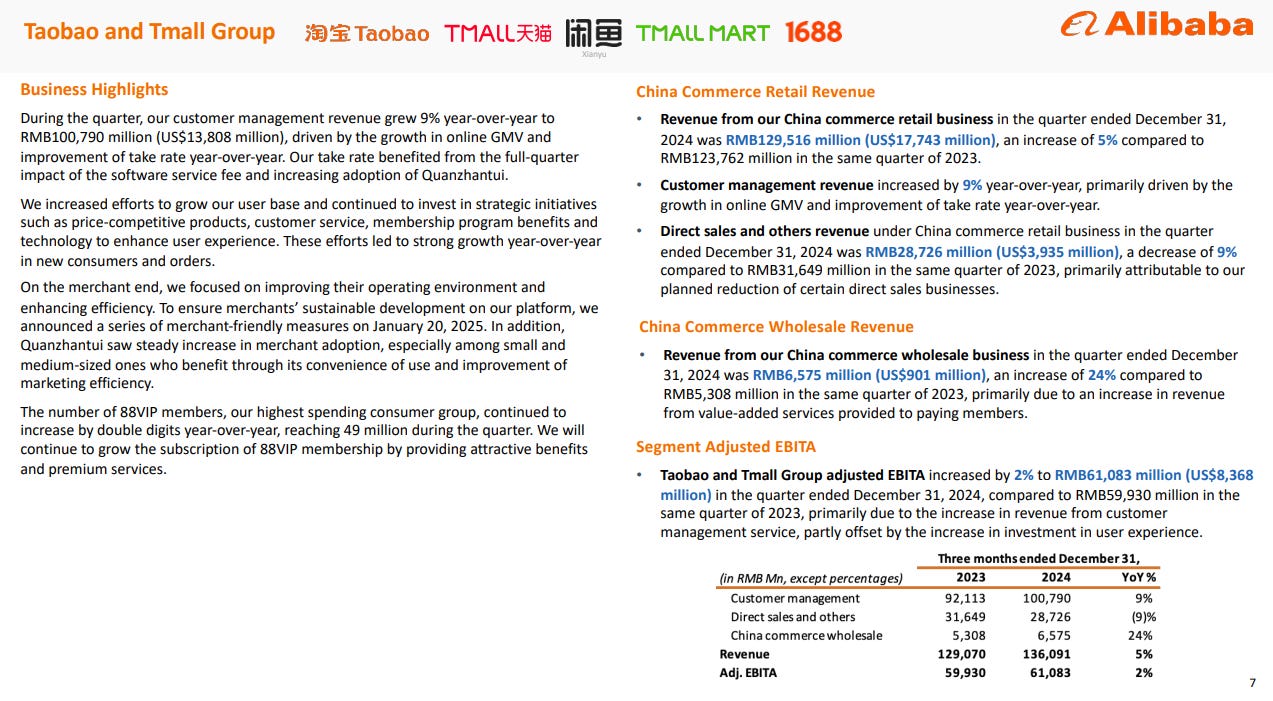

China Commerce Retail (Taobao and Tmall Group):

Combined revenue rose 5% year-over-year to RMB129.52 billion, driven mainly by:

+9% increase in “Customer Management Revenue” (CMR), which includes seller advertising and commissions.

A planned reduction of some direct sales businesses, which weighed slightly on direct sales growth but freed the company to focus more on the marketplace model.

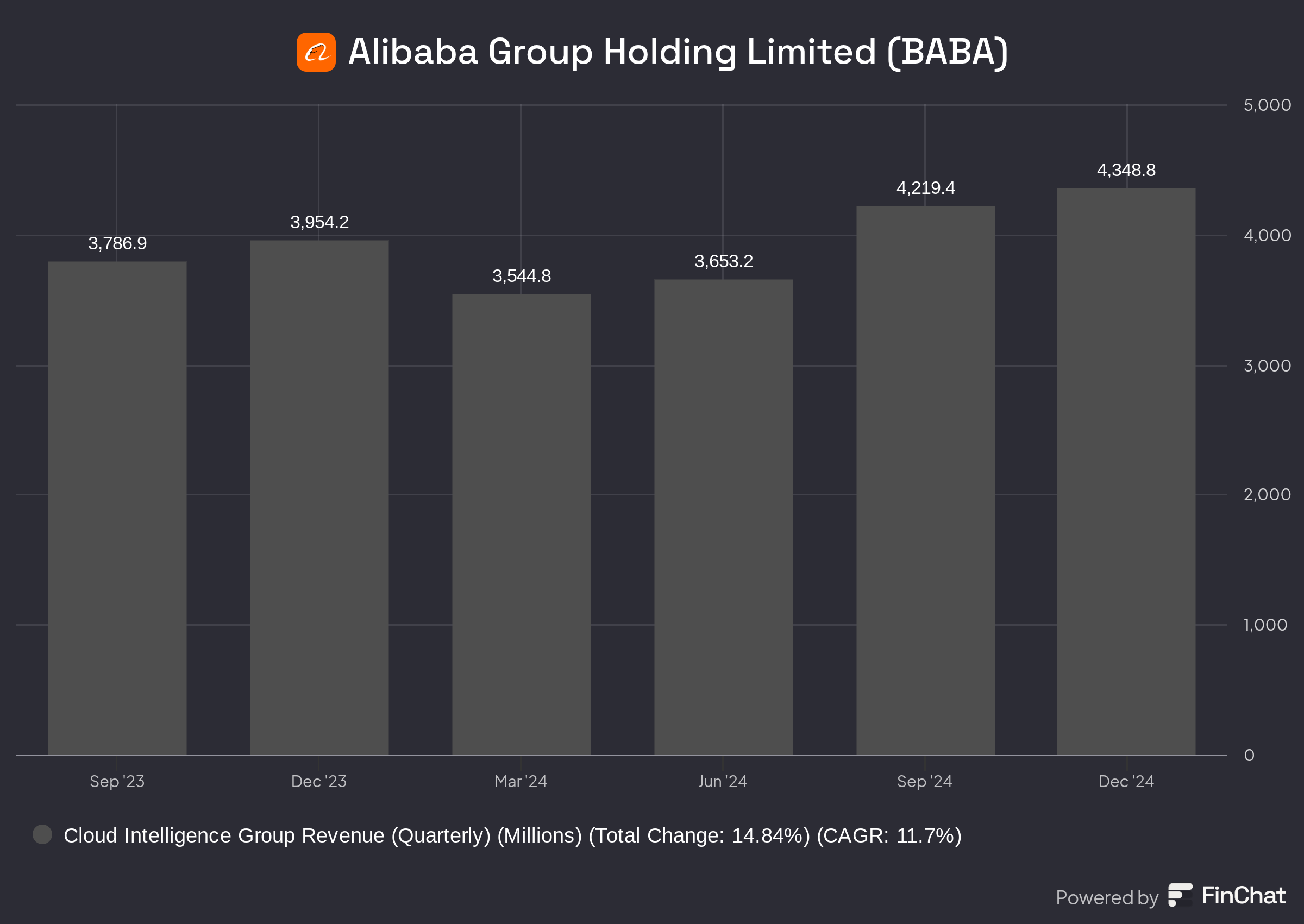

Cloud Intelligence Group:

Revenue grew 13% year-over-year to RMB31.74 billion (US$4.35 billion).

Critically, management pointed out that AI-related product revenue had triple-digit growth for the sixth consecutive quarter.

International Commerce / AIDC:

Revenue up 32% to RMB37.76 billion (US$5.17 billion), with the retail portion (AliExpress, Trendyol, Lazada, etc.) jumping a robust 36% year-over-year.

Management noted AIDC has a clear path to profitability and will become profitable next year. This is extremely important given how large the cross-border market could eventually become.

Adjusted EBITA:

Increased by 4% year-over-year to RMB54.85 billion (US$7.51 billion).

Margins, particularly in the core China commerce segments, benefited from cost controls even as Alibaba stepped up investments in user growth.

Net Income & Cash Position:

Net income attributable to ordinary shareholders soared to RMB48.95 billion (US$6.71 billion).

The company sits on a sizable cash pile of RMB610.04 billion (US$83.58 billion) in cash, short-term investments, and other treasury investments (as of the quarter end).

Even after factoring out some debt, Alibaba’s net cash position remains extremely strong, at well over US$50 billion.

These metrics show that despite macroeconomic uncertainties in China and globally, Alibaba has posted healthy improvements across its major business lines. One theme from management was “accelerating the dragon”—i.e., showing that Alibaba’s big engines (core commerce and cloud computing) were returning to meaningful growth.

2. Domestic Commerce Market Share Stabilizing

One of the standout statements from management this quarter was that Alibaba’s domestic commerce market share is clearly stabilizing. Over the past few years, the market was worried about stiff competition from short-video platforms and other upstarts. We’ve seen live-streaming e-commerce from Douyin (TikTok China) and Kuaishou, for instance, compressing growth rates and causing concerns that Taobao and Tmall might lose their “flagship” status in Chinese e-commerce.

However, looking at recent data:

Taobao and Tmall Group posted a 9% year-over-year increase in CMR (compared to just +2% the quarter prior).

The company’s focus on new merchandising, better user experience, smaller merchants (via simplified ad tools like Quanzhantui), and improved buyer protection has begun to translate into real, positive top-line growth.

The subscription-based loyalty program, 88VIP, now at 49 million members, continues to show promise. These are consumers who have high spending power and likely generate a substantial share of overall GMV.

To me, the biggest takeaway is that Alibaba’s brand equity and ecosystem remain formidable. Moreover, China’s post-pandemic economy is stabilizing.

Management can spend more time enhancing user experience and merchant tools instead of merely playing defense. By focusing on a membership-driven model (88VIP) and by leveraging AI-driven marketing solutions, Alibaba seems intent on returning to sustainable, long-term GMV growth domestically.

From an investor perspective, if you believe in China’s consumption rebound and Alibaba’s ability to hold its e-commerce throne, the re-acceleration of China commerce retail is arguably the single most important piece of the puzzle.

3. International Commerce (AIDC) On Track for Profitability Next Year

Alibaba’s international arm, Alibaba International Digital Commerce Group (AIDC), houses businesses like AliExpress, Trendyol (Turkey), Lazada (Southeast Asia), and various cross-border B2B platforms. While these segments have historically burned cash, the 32% revenue growth this quarter—and, especially, the 36% growth in retail—suggest global demand for Alibaba’s platforms is strong.

Management noted that AIDC increased marketing during shopping festivals, which elevated short-term losses. Nonetheless, certain business lines (e.g., AliExpress’ “Choice” offering) are seeing improved unit economics.

They also mentioned that AIDC will achieve profitability next year, signaling that the heavy investment phase may be peaking.

This is crucial because, as an investor, we need to see a pathway to profit for Alibaba’s major “growth engines,” especially when they require significant cash infusion. AIDC’s eventual profitability would relieve margin pressure and let the group pivot to a self-sustaining, profit-generating pillar.

Strategically, Alibaba’s push into international markets comes at an opportune time:

China’s e-commerce sector is huge and still maturing, but growth has slowed relative to its early days.

In contrast, Southeast Asia, the Middle East, Europe, and select emerging markets might still be in earlier phases of e-commerce adoption.

Alibaba has the logistics experience (via Cainiao) and AI-driven marketing capabilities to make a serious dent in these global markets.

For these reasons, I see AIDC’s upcoming profitability as an extremely bullish sign for the company’s medium to long-term revenue mix and margin expansion.

4. Cloud Intelligence Group: Re-Ignited Growth & AI Emphasis

Alibaba Cloud (now under the “Cloud Intelligence Group”) reported a 13% year-over-year rise in revenue, accelerating from roughly 7% last quarter. The most interesting detail:

AI-related products once again posted triple-digit growth, marking six consecutive quarters of such performance.

Overall Cloud revenue (excluding consolidation effects from Alibaba’s own businesses) rose 11%.

Recent commentary suggests management sees generative AI and high-performance computing as central to the next wave of growth. Alibaba Cloud is also continuing to open-source large language models (the “Qwen” family), which it aims to proliferate widely among enterprises.

Considering the stiff competition in China’s cloud market—from the likes of Tencent Cloud, Huawei Cloud, Baidu AI Cloud—Alibaba’s ability to maintain and re-accelerate growth demonstrates:

The market is far from saturated.

Alibaba’s existing scale, brand, and AI product suite give it a strong advantage in capturing enterprise demand.

Even though Cloud Intelligence Group is not yet at the margins of, say, Amazon Web Services in the U.S., the path to greater profitability is increasingly clear as management scales up high-value product lines (public cloud and AI). Notably, cloud adoption is still lower in China relative to the U.S., meaning the addressable market remains enormous.

5. Cainiao & Logistics

Cainiao, Alibaba’s logistics arm, saw revenue dip slightly by 1% year-over-year to RMB28.24 billion. This was partly due to a restructuring wherein certain logistics platform functions became integrated with the e-commerce businesses.

Cainiao’s adjusted EBITA also declined, as various costs and margin shifts played out. Still, it’s worth emphasizing that Alibaba’s overall shipping network, warehousing footprint, and cross-border capabilities remain second to none in China. Cainiao is vital to ensuring fast, reliable fulfillment for Taobao, Tmall, Freshippo, and the international operations.

Over time, Cainiao’s margin profile could improve if it pivots more aggressively toward external (third-party) clients. Nevertheless, for investors, Cainiao’s role is as much about supporting e-commerce growth as it is about being a standalone business line.

6. Cost Control, Profits, and Shareholder Returns

Alibaba’s management has historically balanced aggressive investment with a focus on margins. The December Quarter results suggest the company is returning to a more balanced strategy:

Adjusted EBITA for the quarter grew 4% year-over-year, thanks in part to cost discipline in China retail and narrowing losses in local services.

Operating margin improved to 15% from 9% a year ago.

Share Repurchases: Alibaba repurchased roughly US$1.3 billion worth of shares during the quarter, underscoring management’s confidence in the company’s valuation and outlook.

Debt Management: The company also issued about US$5 billion in new senior notes at favorable rates, extending maturities.

These moves reflect a conscious effort to optimize capital structure while continuing to return cash to shareholders and invest in strategic growth. As an investor, seeing Alibaba buy back shares near what I perceive as depressed valuations is encouraging.

Moreover, the group’s massive cash balance (over US$50 billion net) positions Alibaba to weather short-term economic turbulence, pursue M&A, or ramp up R&D in AI and Cloud without undue financial stress.

7. China’s Macro Environment and Pro-Business Shift

A critical part of my bullish thesis on Alibaba—and Chinese equities in general—is the emerging shift in government policy from a regulatory clampdown toward a more pro-business stance.

Over the last couple of years, the central government introduced measures targeting everything from fintech to education technology, reining in what was perceived as monopolistic behavior and enforcing data security.

In late 2023, early 2024, and as recently as last week, we began to see a more supportive tone:

Government officials emphasized the importance of “platform economy” players for job creation and economic resilience.

There has been talk of new stimulus or supportive measures to bolster consumer sentiment and re-accelerate consumption.

Key e-commerce events, such as the November 11th “Singles’ Day” (Double 11), remain centerpieces of China’s consumer economy, and the government recognizes that stable or growing demand is vital.

Most recently, a high-profile meeting led by President Xi Jinping with top private-sector entrepreneurs (including Alibaba co-founder Jack Ma and leaders from companies like DeepSeek, BYD, and Tencent) further underscored Beijing’s renewed pro-business outlook

Reassurance to Business Leaders: Xi reassured entrepreneurs that the government’s pro-business approach is anchored in China’s “socialist system with Chinese characteristics,” promising that the legal rights of private companies will be fully protected.

End of Tech Crackdown: The meeting is widely seen as a turning point that marks an end to the severe regulatory clampdowns that began in 2020, which previously stifled innovation and dampened investor confidence.

Boosting Market Confidence: By rehabilitating figures like Jack Ma (who had been sidelined after criticizing regulators) the event aimed to inject renewed confidence among investors and entrepreneurs, suggesting that further supportive measures, including eased financing restrictions, could be on the horizon.

Strategic Economic Support: The gathering underscores Beijing’s recognition that private-sector innovation is crucial for China’s long-term economic growth, particularly as the country faces external pressures such as U.S. tech restrictions and domestic economic challenges.

Management’s statement that domestic commerce market share is stabilizing likely reflects both Alibaba’s own operational improvements and a less hostile regulatory climate. While we shouldn’t discount the competitive environment, a friendlier macro stance from Beijing is a tailwind for Alibaba’s long-term prospects.

8. My Bullish Outlook: Why Alibaba Remains My Largest Position

Market Leader with Multiple Growth Vectors

Alibaba is not just an e-commerce play. It’s a conglomerate spanning cloud computing, international retail, logistics, digital media/entertainment, and more. This diversification means that even if one segment slows, others (e.g., cloud or cross-border commerce) can pick up steam.

Secular Tailwinds

China’s consumer market, although mature in top-tier cities, still has untapped potential in lower-tier cities, rural regions, and specialized product categories. Meanwhile, the global e-commerce market outside China continues to expand, and Alibaba is positioning itself for high-growth geographies.

AIDC Profitability Upside

I’m particularly excited by the prospect that AIDC (Alibaba’s main cross-border commerce segment) is set to be profitable next year. Once that happens, we may see margin expansion and improved sentiment among investors who have previously worried about “money-losing expansions abroad.”

Government Support

The shift to a more pro-business environment in China can’t be overstated. Though no one can precisely predict policy changes, I’m of the view that the government wants to ensure major tech players remain innovative and robust. Alibaba, as a flagship tech company, stands to benefit.

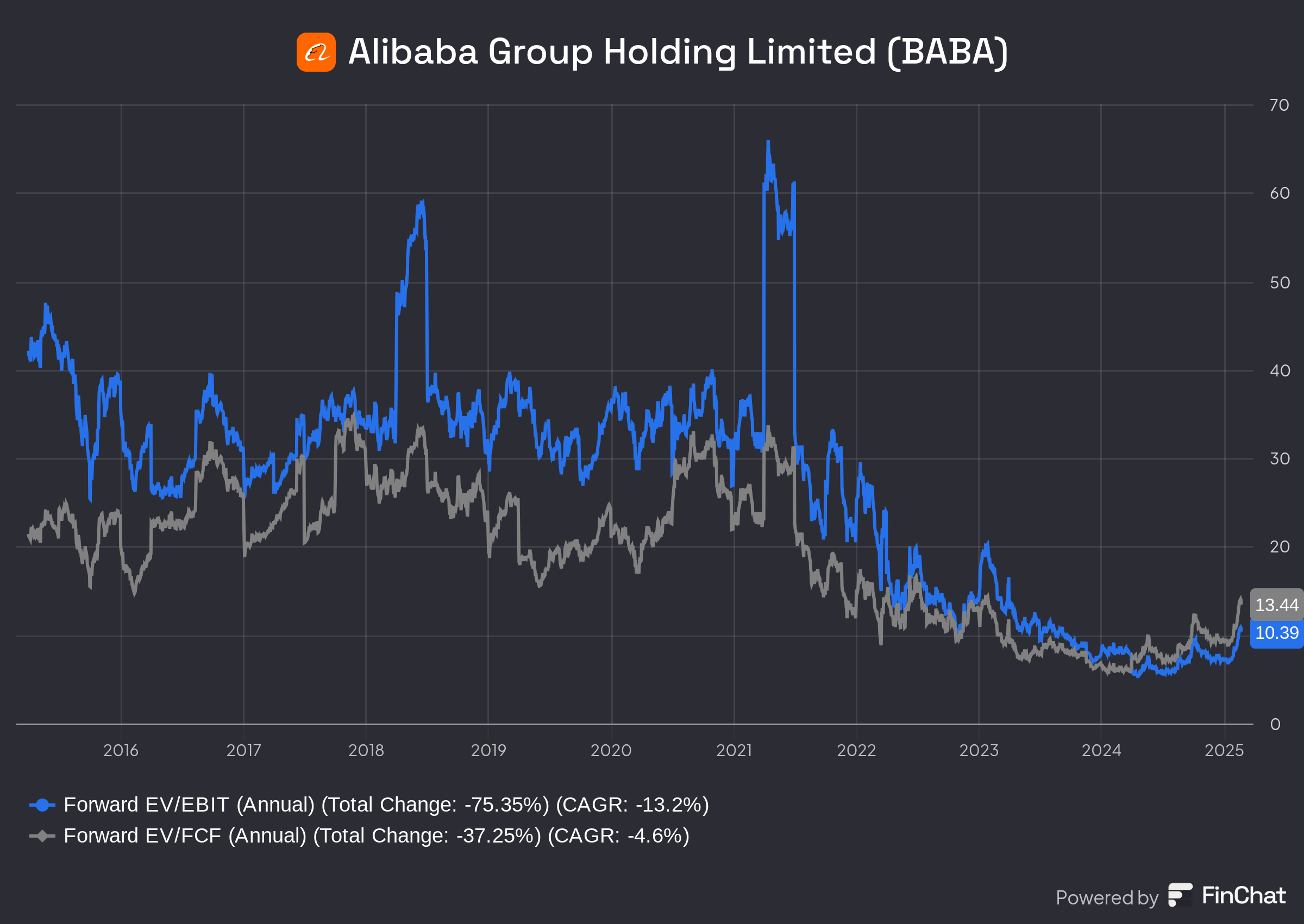

Valuation

Despite the recent massive rally in its stock price, Alibaba continues to trade at what I view as depressed multiples relative to its historical averages and global tech peers. Based on forward estimates:

Forward EV/FCF is around the low-to-mid teens (roughly 13–14x).

Forward EV/EBIT is even lower, hovering around 10–11x.

These multiples have declined sharply (over 70% from their historical peaks) despite the company maintaining its leadership in e-commerce and cloud, generating strong free cash flow (even during a massive investment cycle), and boasting a net cash position of over US$50 billion.

For context, other global e-commerce and cloud leaders (e.g., Amazon) have historically traded at higher multiples, often well above 25x EV/EBIT. While direct comparisons can be tricky due to differences in business mix and geographic risk, Alibaba’s valuation discount seems excessive given:

Renewed Growth: Top-line acceleration in domestic commerce (+9% CMR), cloud computing (+13%), and international commerce (+32%).

AIDC Profitability: The international business is poised to turn profitable next year, potentially lifting overall margins.

AI and Cloud Upside: Alibaba Cloud’s AI-related revenue is growing triple digits, suggesting a long runway for higher-margin products.

Capital Returns: Ongoing share repurchases indicate management sees significant undervaluation.

Improving Regulatory Environment: The worst of the tech crackdown appears behind us, reducing one of the major overhangs that has weighed on the stock’s multiples.

In my view, as Alibaba continues executing across its core and emerging segments, there’s a reasonable path for the market to re-rate the stock closer to historical or peer valuation levels.

Even a modest multiple expansion; say from ~14x forward EV/FCF to ~20-25x could result in substantial upside for shareholders.

9. Risks and Considerations

No investment, of course, is risk-free. For Alibaba, a few potential headwinds linger:

1. Macroeconomic Slowdown: Although the consumer market is stabilizing, any reemergence of major COVID-related restrictions or unexpected economic downturns could hamper discretionary spending.

2. Competition: The domestic e-commerce space, particularly from short-video e-commerce, remains fierce. If Alibaba fails to innovate or adapt, it might lose more share again.

3. Geopolitical Tensions: U.S.-China relations, as well as tensions with other global regions, might impact investor sentiment or impede certain expansion plans.

4. Regulatory Environment: While the tone is currently supportive, regulatory unpredictability is still a factor in the background.

Nonetheless, I believe Alibaba is demonstrating once again that it’s adept at navigating these challenges, supported by extensive resources, strong brand recognition, and an ambitious, tech-savvy management team.

10. Conclusion: “Back to Business”

The Q3 FY2024 earnings underscore a critical inflection point for Alibaba. After a period of regulatory challenges and macro uncertainty, the company is showing re-acceleration in its core segments.

From an investor standpoint, I remain firmly bullish on Alibaba. The company’s fundamental strengths, combined with improving macro conditions and a measured approach to capital allocation, position it for an exciting year ahead.

I believe the next 12–24 months will see Alibaba leverage its new momentum and reaffirm why it became one of the world’s most influential e-commerce and cloud platforms in the first place.

If you’re an investor looking for a high-quality stock with exposure to China, global e-commerce trends, and rapidly evolving AI capabilities, Alibaba makes a compelling case. Yes, challenges remain. But after reviewing these results, it’s hard to deny the feeling that Alibaba has finally turned the corner.

Disclosure: I am long Alibaba with a position that constitutes about 20% of my overall portfolio. I also hold other Chinese equities and believe in China’s long-term consumer growth story. Please note this post reflects my personal opinions and does not constitute financial advice. Always do your own due diligence and consider your individual financial goals and risk tolerance before making any investment decision.