Deep Dive into British American Tobacco (BTI)

82% Profit Margins, 7% Dividend Yield, Trading at 7.3x FCF

The story of tobacco in the 21st century is one of existential crisis and audacious reinvention. With smoking rates in terminal decline and regulators turning the screws, cigarette giants find themselves at a crossroads: adapt or die.

Enter British American Tobacco, the 120-year-old behemoth best known for iconic brands like Lucky Strike and Pall Mall. While still churning out hundreds of billions of cigarettes annually and generating billions in cash, management recognizes the writing on the wall.

Their solution? A full-throttle pivot into smoke-free alternatives, headlined by the rapidly growing nicotine pouch category.

Leading that charge is VELO, BAT's flagship nicotine pouch brand, which is posting phenomenal growth globally and gaining significant traction in the US following the launch of VELO Plus in December 2024. With the nicotine pouch market projected to expand at a sizzling 30% CAGR through 2031, BAT appears well-positioned to ride this disruptive wave.

This shift from a dedicated cigarette supporter to a proponent of a smoke-free future is filled with challenges and contradictions.

Can a company that built its empire on traditional smokes really lead the charge into a tobacco-free future? Will consumers and regulators buy into BAT's metamorphosis? And most crucially for investors, does the current valuation adequately reflect the magnitude of the opportunity ahead?

This deep dive aims to unpack these questions and more. We'll briefly look into BAT's history, dissect its rapidly evolving business model, evaluate the potential of its New Category products, and examine the capabilities of the management team steering this ship through uncharted waters.

Company History

Picture it: 1902. The British Empire is at its height, and smoking is the coolest thing since top hats. Into this world is born British American Tobacco, the lovechild of the UK's Imperial Tobacco and the American Tobacco Company.

Over the next century, BAT would become an empire of its own, gobbling up brands like Lucky Strike, Pall Mall, and Rothmans as it colonized the globe. With a footprint spanning 180 countries, BAT built a reputation as the quintessential tobacco giant, churning out trillions of cigarettes to loyal smokers from London to Lagos.

But as the 20th century drew to a close, storm clouds were gathering. Science had firmly linked smoking to cancer, and lawsuits were mounting. Governments started slapping warning labels and ad restrictions on cigarette packs. The percentage of adults who smoked began to decline, first in the developed world, then in emerging markets.

BAT saw the writing on the wall. They couldn't just keep riding the cigarette train forever. They needed a new playbook.

Enter the 2020s, and BAT's audacious bet on a smoke-free future. The company is pouring billions into new categories like vaping, heated tobacco, and nicotine pouches, with the goal of hitting £5 billion in "New Category" revenue by 2025 and 50 million non-combustible product consumers by 2030.

It's a bold vision, and one that's still very much a work in progress. But if BAT can pull it off, it could mark a new chapter in the company's long and winding history.

Business Overview

So, how exactly does BAT make money? At a high level, it's a pretty simple business. BAT sells nicotine products to consumers, mainly through retail channels like convenience stores, gas stations, and tobacco shops.

Historically, the vast majority of those sales have been cigarettes, sold under brands like Dunhill, Kent, Lucky Strike, Pall Mall, Rothmans, Newport, and Natural American Spirit.

The economics of the cigarette business are incredibly attractive.

Cigarettes enjoy massive manufacturing scale economies, with billions of units produced annually on highly automated production lines. Distribution is also highly efficient, with products moving through a well-established network of wholesalers and retailers. And pricing power is off the charts, thanks to the addictive nature of nicotine and the brand loyalty smokers tend to exhibit.

As a result, BAT has long enjoyed mouth-wateringly high margins, with operating margins hovering in the 30-40% range. Even as cigarette volumes have slowly declined in recent years, BAT has been able to keep profits chugging along by cutting costs and raising prices.

Over the past decade, BAT's revenue has grown at a 6% CAGR, while EBIT has compounded at a 7% clip.

Level up your investment research with Koyfin's powerful market analytics platform. I've been using their comprehensive dashboards, real-time data, and intuitive charting tools to make more informed financial decisions. Try Koyfin today using my referral link and get 20% OFF any paid plan.

Try Koyfin Now!

But here's the thing: that growth algorithm is getting harder to sustain.

Cigarette volumes are falling faster as more smokers quit or switch to alternatives. Governments are getting more aggressive with excise taxes and marketing restrictions. And competition is heating up, both from other tobacco giants like Philip Morris International (PM) and Altria (MO), and from upstart vaping brands like Juul and NJOY.

That's where BAT's "New Categories" come in. The company is betting big on smoke-free products like vapes (Vuse), heated tobacco (glo), and nicotine pouches (Velo).

These products still deliver nicotine, but without the combustion and tar that make cigarettes so harmful. The idea is that as smokers ditch traditional cigarettes, BAT will be there to catch them with a full range of satisfying alternatives.

While these products still contain nicotine and aren't risk-free, most scientists agree they are far less harmful than traditional cigarettes. Public Health England, for example, has concluded that vaping is at least 95% safer than smoking.

For BAT, these new categories represent a huge growth opportunity. The global vapor market is already worth over $20 billion annually and is growing at a double-digit clip. The heated tobacco category is smaller but growing even faster, with sales nearly doubling in 2024. And while nicotine pouches are the newest category, they're also the most promising, with the potential to reach a broader audience of adult nicotine consumers.

So that's BAT's playbook in a nutshell. Milk the cash cow cigarette business for all it's worth, while simultaneously investing billions to build the smoke-free brands of the future. It's a tricky balancing act, but one that BAT believes will allow it to generate robust cash flows today while still positioning itself for long-term growth.

Growth Potential

Now let's talk numbers. Just how big could these "New Categories" get for BAT, and how fast could they get there? The short answer is: pretty darn big, and pretty darn fast.

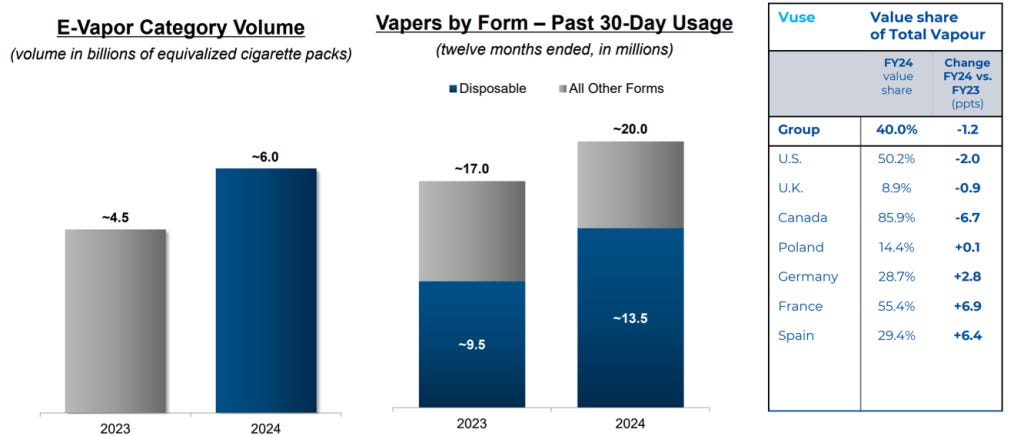

1. Vaping (Vuse)

BAT's Vuse brand is already the global vaping leader, with significant market presence across key regions. In 2024, Vuse generated £1.7 billion in revenue, establishing itself as BAT's largest smokeless category.

Performance has been mixed recently, with volume declining 5.9% and adjusted revenue down 2.5% in 2024. This underperformance stems primarily from:

Lack of enforcement against illegal flavored disposable vapes in the US

Similar challenges in Quebec, Canada

Competition from single-use products that bypass regulations

Despite these headwinds, Vuse maintains its leadership position outside the US and remains the market leader in the legal portion of the US market, which comprises roughly 20% of the total vapor category by value. The illegal portion represents a staggering 60% of the market, indicating significant potential for recovery once enforcement improves.

Looking ahead, BAT is planning to roll out new Vuse innovations in the second half of 2025, which they expect will reinvigorate performance. Marroco highlighted these new launches as key drivers of anticipated double-digit growth in New Categories revenue during H2 2025.

The real prize remains the US, which accounts for over half of global vapor sales. If regulatory enforcement strengthens as expected in early 2025, Vuse could recover meaningful market share from the $10 billion total vapor market.

2. Heated Tobacco (glo)

BAT's heated tobacco business represents a critical pillar in their transformation strategy, though it faces unique challenges compared to their other smokeless categories. In 2024, glo generated £0.9 billion in revenue, positioning BAT as the global #2 player behind Philip Morris International's IQOS.

Performance has been relatively flat, with volume down marginally (-0.3%) in 2024 while adjusted revenue grew by +5.8%. BAT lost 40 basis points of market share in their top 9 markets, bringing their total heated tobacco share to 16.7%. Regional performance varies significantly, with share gains in Poland and Czechia, stabilization in Italy, but ongoing competitive pressure in Japan and South Korea.

BAT's heated tobacco strategy is now two-pronged:

Glo Hyper Pro: Launched in 2024, this device competes in the "affordable segment" (~20% of category value)

Glo Hilo: Their upcoming premium device aimed at challenging IQOS Iluma (targeting the premium segment that comprises 80% of category value)

The company has also innovated with "veo," a non-tobacco heated product in Europe that's reportedly outperforming competitors. This demonstrates BAT's willingness to diversify beyond traditional tobacco-based offerings.

Despite making heated tobacco improvement a strategic priority, this remains BAT's most challenged smokeless category. The success of Glo Hilo will be particularly critical to watch, as it represents BAT's first serious attempt to compete in the premium heated tobacco segment.

3. Nicotine Pouches (VELO)

The real wildcard in BAT's transformation is modern oral nicotine pouches. This category has delivered standout performance, with volumes surging 56.1% and adjusted revenue up 53.2% in 2024. VELO now serves 7.4 million users globally, with average daily consumption increasing across the board.

VELO's performance has been particularly impressive in the US market, where volume grew an astonishing 234% and revenue jumped 223% in 2024. This growth has accelerated into early 2025, largely due to the successful December 2024 launch of VELO Plus. According to the latest Nielsen data from March 2025:

VELO's 4-week rolling volume share reached 7.9% nationally, representing 185% year-on-year growth

The most recent weekly measurements show VELO approaching 10% share

VELO Plus captured 5.4% national share within just 12 weeks of introduction

VELO Plus now accounts for approximately 70% of total VELO volume

What makes VELO Plus so compelling? It addresses key consumer preferences with:

Larger, softer and "wet" (higher moisture content) pouches compared to the "dry" format of category leader ZYN

Higher nicotine strengths (6mg and 9mg) for greater satisfaction

Competitive pricing at $2.99 for a can of 20 pouches (versus ZYN's $5.59 for 15 pouches)

Expanded flavor range with Mint, Spearmint, Peppermint, Wintergreen, Wild Berry, and Citrus Chill options

Meanwhile, category leader ZYN has seen its growth rate slow to just 13.2% year-on-year, with market share dipping toward 55%. This suggests VELO's gains are coming partly at ZYN's expense.

BAT is aggressively expanding VELO Plus distribution from 75,000 to 110,000 US stores by April 2025, though this still trails ZYN's presence in 140,000 locations. Longer-term, BAT awaits FDA approval for their European VELO 2.0 product, which has demonstrated strong performance internationally.

The global nicotine pouch market is projected to grow at a CAGR of 27-34% (depending on the estimate), potentially reaching $22-28 billion by 2030-2033. With VELO's momentum and BAT's distribution capabilities, this category represents their most promising growth avenue.

Adding it all up, I believe BAT's New Categories could hit £5 billion by 2025 (up from £3.4 billion in 2024) and continue growing at a healthy clip thereafter. That would represent a significant chunk of BAT's total revenues, a massive shift from sub-5% in 2017.

Of course, this assumes Vuse recovers with improved enforcement, VELO continues its remarkable trajectory, and glo makes meaningful progress against IQOS. But the opportunity is immense, and BAT appears to be executing particularly well in the fast-growing modern oral segment.

Evaluation of Management Quality

Of course, a great business model is nothing without great people to execute it. So let's take a closer look at the folks steering the ship at BAT.

CEO Tadeu Marroco took over in 2023 and has been with the company for decades. He's been instrumental in driving BAT's "A Better Tomorrow" strategy, focusing on transforming the business toward smokeless products. Under his leadership, BAT has emphasized "Quality Growth" – balancing top-line expansion with profitability improvement in New Categories.

Marroco is surrounded by a deep bench of talented leaders, many of whom have been with BAT for decades. But the company has also been strategic about bringing in outside talent to boost capabilities in areas like technology, marketing, and R&D. This kind of "cross-pollination" is valuable for injecting fresh thinking into a large organization.

BAT also seems to have a strong culture of talent development, with robust leadership training programs and an emphasis on promoting from within. The company consistently earns high marks from employees on sites like Glassdoor, with many praising the competitive pay, collaborative culture, and growth opportunities.

Of course, the proof will be in the pudding. BAT's leadership team faces immense challenges in pivoting to smoke-free products while keeping the core business humming. They need to build winning brands in completely new categories while navigating complex regulations across dozens of markets. It won't be easy.

But I'm encouraged by the experience and skills of Marroco and his team. They seem to have a credible plan and aren't afraid to make bold moves to shape BAT's destiny. While there will surely be speed bumps, I believe this is a management team built for the long haul.

Valuation

Now for the million dollar question: what's BAT actually worth?

The stock currently trades around 8.9x NTM earnings and 7.2x FCF, a significant discount to both historical averages and tobacco peers. Philip Morris International, by comparison, trades at about 22x NTM earnings despite similar growth challenges in its traditional cigarette business.

Why the discount? Tobacco stocks in general have been de-rated in recent years as ESG-conscious investors swear off the sector. The regulatory clouds are only darkening, with flavored vape bans and nicotine caps on the table. And of course, there's the perpetual decline of cigarette volumes as more smokers kick the habit. All of this has led to a "tobacco discount" in the market.

But the valuation gap between BAT and Philip Morris seems excessive.

Yes, PM has a head start in heated tobacco with IQOS as well as nicotine pouches with ZYN, but BAT is leading in global vaping and gaining ground rapidly in nicotine pouches. BAT also offers a significantly higher dividend yield (7% vs. PM's 5%) and has a more active share repurchase program.

Even Altria, which faces many of the same challenges as BAT in the US market, trades at a premium at about 11x earnings. Imperial Brands, arguably the least advanced in next-gen products, commands a 9x multiple.

I'd argue the discount is overdone in BAT's case. The company has industry-leading margins, generates mountains of cash, and pays a well-covered 7% dividend. With £900 million in buybacks planned for 2025 and leverage at a comfortable 2.4x, there's ample capacity to reward shareholders while still investing for growth.

The key question is what kind of earnings power BAT will have in the future as cigarettes become a smaller piece of the pie. Bulls think New Categories can fully offset cigarette declines, keeping EPS chugging along. Bears see a classic "melting ice cube" that will struggle to maintain profits as volumes shrink.

Personally, I'm somewhere in the middle. I believe BAT's New Categories will be very successful, but not enough to keep the overall pie from shrinking a bit. My base case assumes cigarette volumes keep declining at a moderate pace, vapor grows at a healthy clip, and heated tobacco and pouches become multi-billion dollar businesses.

Put a more reasonable multiple on BAT (let's say 12x, still a discount to global staples companies and peers) and you'd see significant upside from today's levels. Add in the dividends and you're looking at a potentially attractive total return.

The upside scenario is that New Categories really take off, allowing BAT to more than replace cigarette profits and drive sustained EPS growth. If that happens and the market awards a higher multiple, the stock could have tremendous upside.

The bear case is that cigarette volumes fall off a cliff, vaping growth stalls out, and heated tobacco/pouches fail to scale. If that happens and investors still shun tobacco, we could see downside from here.

For me, the skew seems to the upside. A lot would have to go wrong for BAT to be permanently impaired. Even if the next few years are bumpy, the core business is so cash-generative that I believe BAT will have the resources to keep investing and adapting. And at today's price, you're getting paid a hefty dividend while you wait for the transformation to play out.

Concluding Thoughts

Putting it all together, I see British American Tobacco as a classic "value with a catalyst" play. The core tobacco business is a cash machine, the balance sheet is strong, and the dividend is attractive. But the real juice is the shift to smoke-free, particularly the rapidly growing nicotine pouch segment where VELO Plus is showing encouraging early results.

While the next few years may be bumpy, I'm confident this management team has the brands and strategy to make BAT a leader in vaping, heated tobacco, and modern oral.

At 8.9x earnings and with a 7% dividend yield, it seems the market is pricing in an awful lot of pessimism. I see a business still capable of generating steady profits while investing for an attractive future. With some luck and solid execution, I believe BAT shares can deliver solid returns from here.

But hey, that's just my opinion.

Maybe I'll end up sounding like an idiot. Wouldn't be the first time, and I'm sure it won't be the last! As always, I'm eager to hear your take. Let me know in the comments what I'm missing. Whoever you are, wherever you are, I hope this was a stimulating read.

Nice write up!

BTI is on my watchlist. Might be time to give them another look.

Well written and clear! But they lost me when they acquired Reynolds, waste of money for a business they were already controlling. That strategy of consolidating minorities was expensive and not value adding. I still prefer PMI given their leadership position in HNB, cannot disagree with the valuation gap though!