Is Palantir a Bubble?

Why This High-Flying Tech Stock Might Be Dangerously Overvalued

“A great company is not a great investment if you pay too much for the stock.” — Benjamin Graham

Palantir Technologies (PLTR) has been one of the hottest stocks in the market. The data analytics company, known for its secretive work with government agencies, has seen its share price surge as investors pile into the narrative of AI-driven growth. But beneath the hype lies a stark reality: Palantir is dangerously overvalued, and its current valuation is bordering on the absurd. While Palantir may be a great company with impressive technology, its stock price has become completely detached from fundamentals, making it a risky and likely poor investment at current levels.

A Brief History of Palantir

Founded in 2003 by Peter Thiel, Alex Karp, Joe Lonsdale, Stephen Cohen, and Nathan Gettings, Palantir's initial mission was to build software that could help intelligence agencies like the CIA analyze vast amounts of data to identify terrorist threats. The company's name itself, inspired by the all-seeing stones in The Lord of the Rings, reflects its ambitious goal of providing unparalleled insight from complex datasets.

For years, Palantir operated largely in the shadows, building its reputation through its work with government agencies. The company's flagship product, Gotham, became a crucial tool for intelligence and law enforcement agencies worldwide. In the late 2000s, Palantir expanded into the commercial sector with Foundry, a platform designed to help businesses manage and analyze their data.

After years of anticipation, Palantir finally went public in September 2020 through a direct listing. The IPO was met with significant investor interest, but the stock experienced a relatively muted debut. However, since then, particularly in recent months, the stock has skyrocketed, driven by investor enthusiasm for AI and the company's expanding commercial business.

The Elephant in the Room: An Egregious Valuation

While Palantir's story is compelling, its financial metrics paint a different picture, one of a company priced for a level of perfection that is virtually unattainable.

Palantir currently trades at a staggering >60x TTM sales & ~400x TTM P/E. To put this into perspective, the average P/S ratio for software companies is closer to 7-9x. Even other high-growth SaaS companies rarely trade above 20x sales. A ~60x P/S ratio implies that investors are paying $60 for every $1 of revenue Palantir generates. This is an absurd multiple that suggests an EXTREMELY optimistic view on future growth, margin expansion, or a combination of both.

While Palantir has demonstrated respectable revenue growth, a closer look reveals that it's not expanding at a pace that aligns with its current valuation. In 2024, the company recorded a 24% year-over-year revenue increase, a figure that might seem impressive at first glance. However, considering that Palantir is currently trading at a price-to-sales (P/S) multiple of ~60x, this growth rate falls short of expectations.

Essentially, investors at this valuation are implicitly betting on decades of hyper-growth, a scenario that appears highly improbable given Palantir's already substantial revenue base and the increasingly competitive landscape in which it operates. To justify its current valuation, Palantir would need to consistently achieve revenue growth in the 40-50% range for many years to come, a feat that seems increasingly challenging.

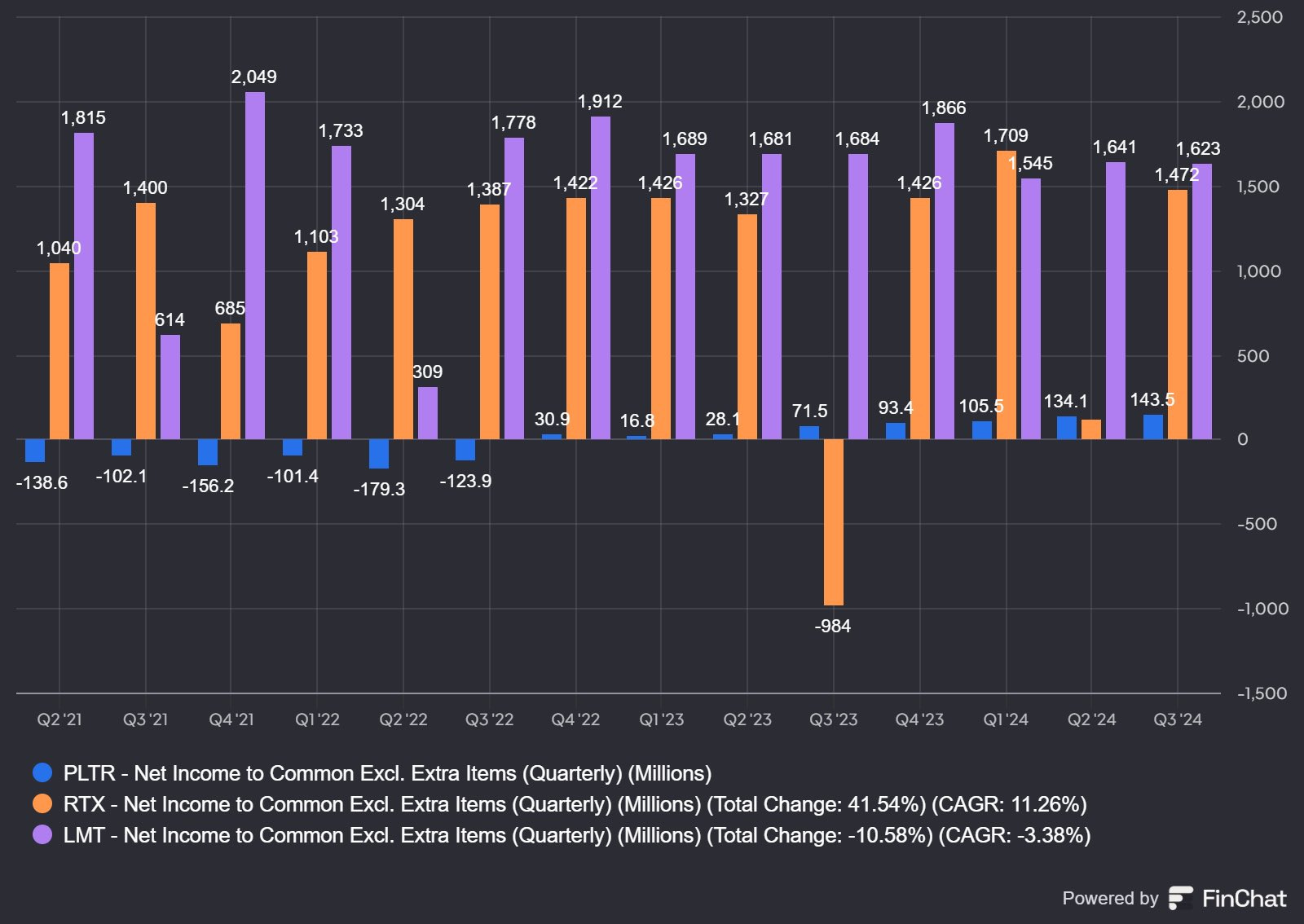

Furthermore, Palantir's profitability raises concerns. Despite reporting $476 million in net income, almost $200 million of this amount stemmed from interest income, not its core operations. More alarmingly, the company disclosed a staggering $540 million in stock-based compensation (SBC) expenses. This high level of SBC not only dilutes existing shareholders' ownership but also raises questions about the company's long-term profitability prospects.

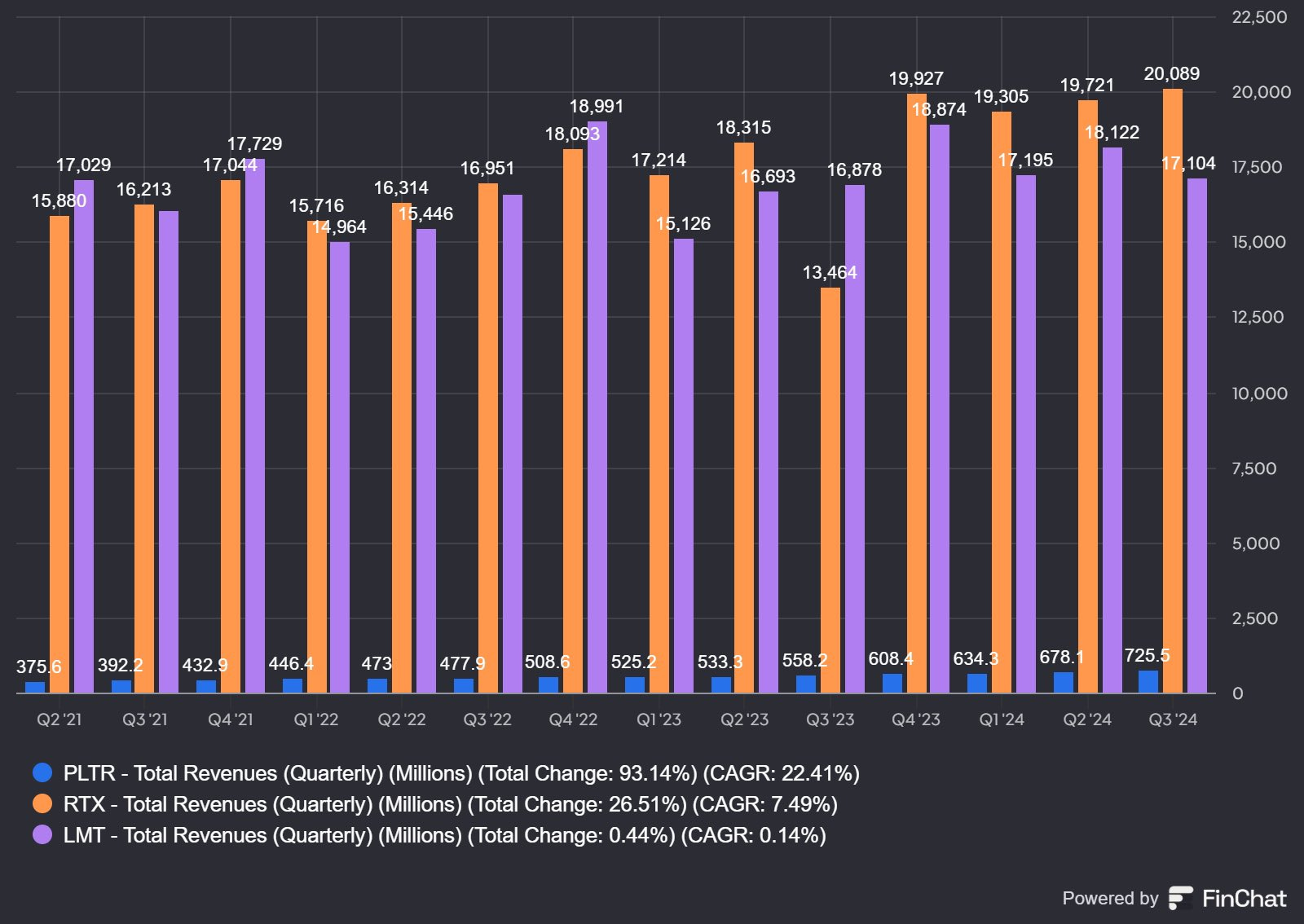

With a market cap of over $150 billion, Palantir is now valued more than many established giants like LMT 0.00%↑ and RTX 0.00%↑ who have significantly higher revenues and profits. It is priced like a dominant, mature defense contractor/tech leader, but it's still a relatively young company with a long way to go to prove its long-term profitability and market dominance.

A History of High-Flying Stocks and Their Eventual Fall from Grace

Palantir's current valuation, with its lofty price-to-sales multiple, brings to mind a long history of companies that soared to seemingly unsustainable heights, only to come crashing back down to earth. While past performance is not indicative of future results, it's important to understand these historical trends to gain perspective on Palantir's potential trajectory.

Throughout the dot-com bubble of the late 1990s, numerous internet companies with unproven business models and limited revenue traded at astronomical valuations. Companies like Pets.com and Webvan, fueled by speculative fervor, reached incredible market capitalizations before ultimately collapsing as the bubble burst. Similarly, the recent SPAC boom saw many companies go public with sky-high valuations based on little more than promises of future growth. Many of these companies have since seen their stock prices plummet as the initial hype subsided and the realities of their businesses set in.

Even established tech giants are not immune to this phenomenon. In the early 2000s, Cisco Systems, a leader in networking equipment, traded at a P/S ratio exceeding 100x. While Cisco ultimately survived the dot-com crash, its stock price languished for years as it struggled to grow into its inflated valuation. More recently, companies like Zoom and Peloton experienced meteoric rises during the pandemic, only to see their valuations contract significantly as growth slowed and investor enthusiasm waned.

While periods of hyper-growth and investor exuberance can drive valuations to extraordinary levels, gravity eventually takes hold. Companies that fail to deliver sustained growth and profitability often face a painful reckoning. For Palantir to defy this historical trend, it will need to demonstrate exceptional execution and consistently exceed the lofty expectations embedded in its current valuation.

Great Company ≠ Great Investment

It's crucial to separate the quality of a company from the attractiveness of its stock. Palantir undoubtedly has cutting-edge technology and a strong foothold in both the government and commercial sectors. The company's ability to help organizations make sense of complex data is valuable, and its long-term potential is undeniable.

However, a great company does not automatically translate into a great investment, especially when the stock is priced at such an extreme valuation. Investors buying $PLTR at current levels are essentially betting that Palantir will not only continue to grow rapidly but also achieve levels of profitability and market dominance that are rare even among the most successful technology companies.

Palantir is a fascinating company with impressive technology, but its stock is simply too expensive. Investors buying Palantir at ~60x sales are taking on an enormous amount of risk for a potentially very limited reward. While the company may continue to grow and succeed, it's highly unlikely that it will be able to live up to the extreme expectations baked into its current valuation.

For now, investors would be wise to steer clear of Palantir. There are many other companies in the tech sector with more reasonable valuations and equally compelling growth prospects. Wait for a significant pullback before even considering an investment in Palantir. The current price is simply too high to justify, even for a company with Palantir's potential. Remember, even the best companies can be terrible investments if the price is wrong. And right now, Palantir's price is very, very wrong.

Great article -- Palantir is ridiculous. SBC is crazy, management is selling shares, people don't even know what it does.

Not a bubble. Definitely overvalued.