Mature SaaS Business trading at 11x EBIT; 33% FCF Margin; 29% ROCE; Repurchasing Stock

A business with a proven, high-margin recurring revenue model that not only generates but consistently grows free cash flow.

In a world where we’re constantly chasing the next big, flashy innovation, sometimes the simplest ideas are the best ones. The business we’ll be talking about today might not be the tech superstar grabbing all the headlines, but its steady, reliable service has made it a trusted name for millions of users worldwide. In this post, I’ll explain why this “boring” yet solid investment is a very compelling opportunity. After all, sometimes the best opportunities are the ones that quietly deliver consistent results over time.

The investment idea is straightforward. We’re looking at a business with a proven, high-margin recurring revenue model that not only generates but consistently grows free cash flow. It also uses share buybacks to reduce its share count, all while trading at an attractive valuation. In my view, these factors combine to offer significant upside potential in the years ahead.

Investment Overview

Dropbox isn’t simply a cloud storage provider—it’s a company that has smartly evolved its core offering into a diversified cloud software business. While most investors peg Dropbox as a straightforward storage product, the firm has strategically augmented its core business with product enhancements and select acquisitions. This approach not only deepens its service offerings but also creates additional value for both existing and prospective customers. In my view, this diversified model, combined with strong financial discipline, makes Dropbox an attractive compounder poised to deliver steady growth over the coming years.

Competitive Positioning and Market Misunderstanding

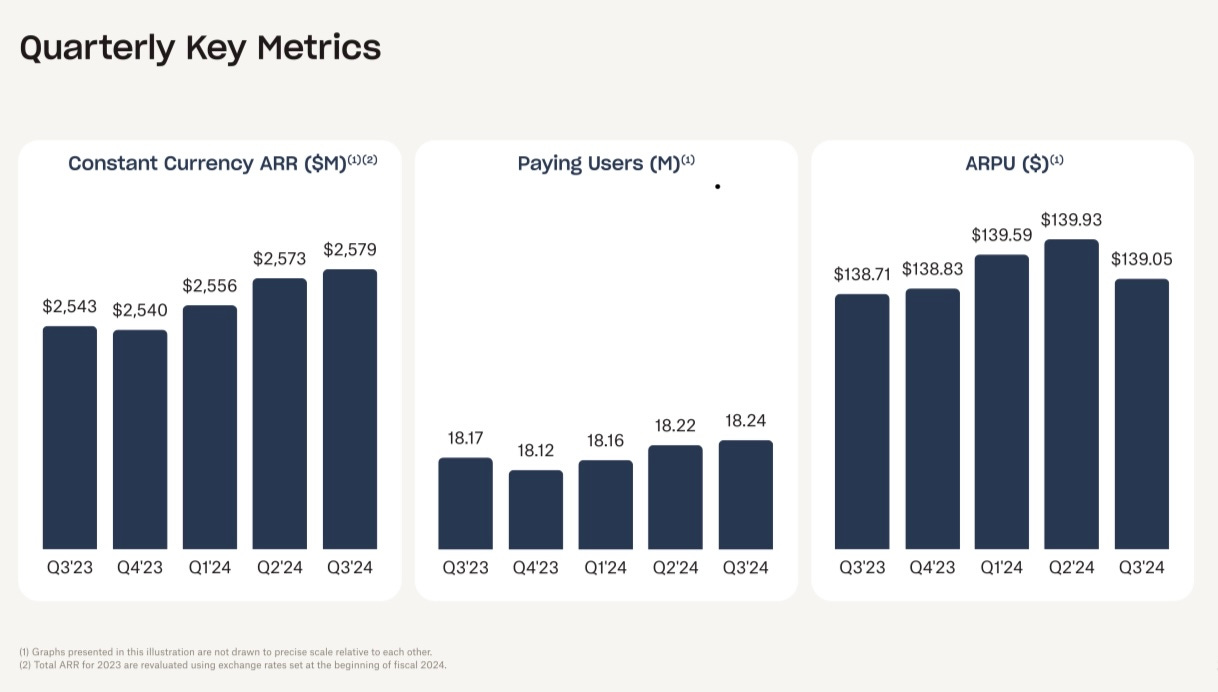

Despite its transformation, the market often still lumps Dropbox into the “commodity storage” category alongside giants like Microsoft and Google. Yet, Dropbox’s performance metrics tell a more nuanced story. Its net revenue retention rate remains around 90%, underscoring both the stickiness of its product and the recurring nature of its revenue.

What’s more, Dropbox continues to expand its paying user base—from 15.48M in 2020 to >18M in 2023—while also steadily increasing ARPU (Average Revenue Per User). ARPU rose from $128.50 in 2020 to $139.38 in 2023. This growth in per-user revenue, combined with a high retention rate, shows that Dropbox has been effective in capturing more value from its established customers rather than merely relying on new signups from its massive registered user base of over 700M.

Even if Dropbox lacks the sheer scale or diversified product suites of larger rivals, its disciplined approach to innovation and targeted product enhancements underpins durable revenue streams. The gap between how the market typically perceives Dropbox and what its metrics actually show remains wide. By leveraging strong customer loyalty and methodical ARPU growth, Dropbox continues to demonstrate that it is more than just a “low-differentiation storage player.” Its fundamental strengths position it well for long-term resilience and the possibility of further market-share gains, even if broader sentiment has yet to catch up with the numbers.

Keep reading with a 7-day free trial

Subscribe to Coughlin Capital to keep reading this post and get 7 days of free access to the full post archives.