3 Stocks I’m Watching This Month

A new monthly series: Watchlist with commentary

Level up your investment research with Koyfin's powerful market analytics platform. I've been using their comprehensive dashboards, real-time data, and intuitive charting tools to make more informed financial decisions. Try Koyfin today using my referral link and get 20% OFF any paid plan.

Kicking off something new today: Each month, I'll share a handful of stocks that have earned a spot on my radar—sometimes because the business is changing, sometimes because the price is. But let me set expectations up front: most of these names will never make it into my portfolio.

If you've followed me for any length of time, you know I don't swing at many pitches. I run a concentrated book and am painfully slow to add new positions. Most of my capital sits in a small handful of companies I know inside and out, and I'll happily watch dozens of stocks for years before ever making a move. It's not flashy, but it's the only way I know how to compound with conviction.

So why do this series at all?

Because in a market this noisy, I think there's real value in periodically zooming out—spotting where sentiment, business fundamentals, or valuations have shifted enough to warrant a second look. Sometimes these will be blue-chip names everyone's heard of. Other times, it'll be an under-the-radar stock getting ignored by almost everyone but me. Either way, think of this as a running "watchlist with commentary"—not a buy list, and definitely not investment advice.

Some months, the companies I mention will quietly disappear from future updates. Occasionally, one will make the cut for a full deep dive and maybe, just maybe, a spot in my own portfolio. For now, here are three companies I'm watching as we start June, and why they stand out.

Fair Isaac Corp ($FICO) - The Credit Score Monopoly

FICO owns credit scoring in America. When you apply for a mortgage, car loan, or credit card, lenders use FICO scores to decide whether you're worth the risk.

They've spent 70 years building this moat, and it's basically insurmountable now.

The recent selloff caught my attention. The stock has fallen roughly 27% from its November 2024 peak, creating the kind of opportunity that rarely appears in a name this dominant.

Here's a company that's been raising prices on an essential service for decades—they just bumped their mortgage score price from $3.50 to $4.95 for 2025, and lenders just grumbled and paid up.

Try doing that in any other industry.

The real story is their software business. While everyone focuses on the credit scores, FICO has been quietly building decision management platforms that help banks automate lending decisions.

This segment is growing 15-20% annually and carries much higher margins than legacy scoring. They're selling the pick and the shovel in the credit gold rush.

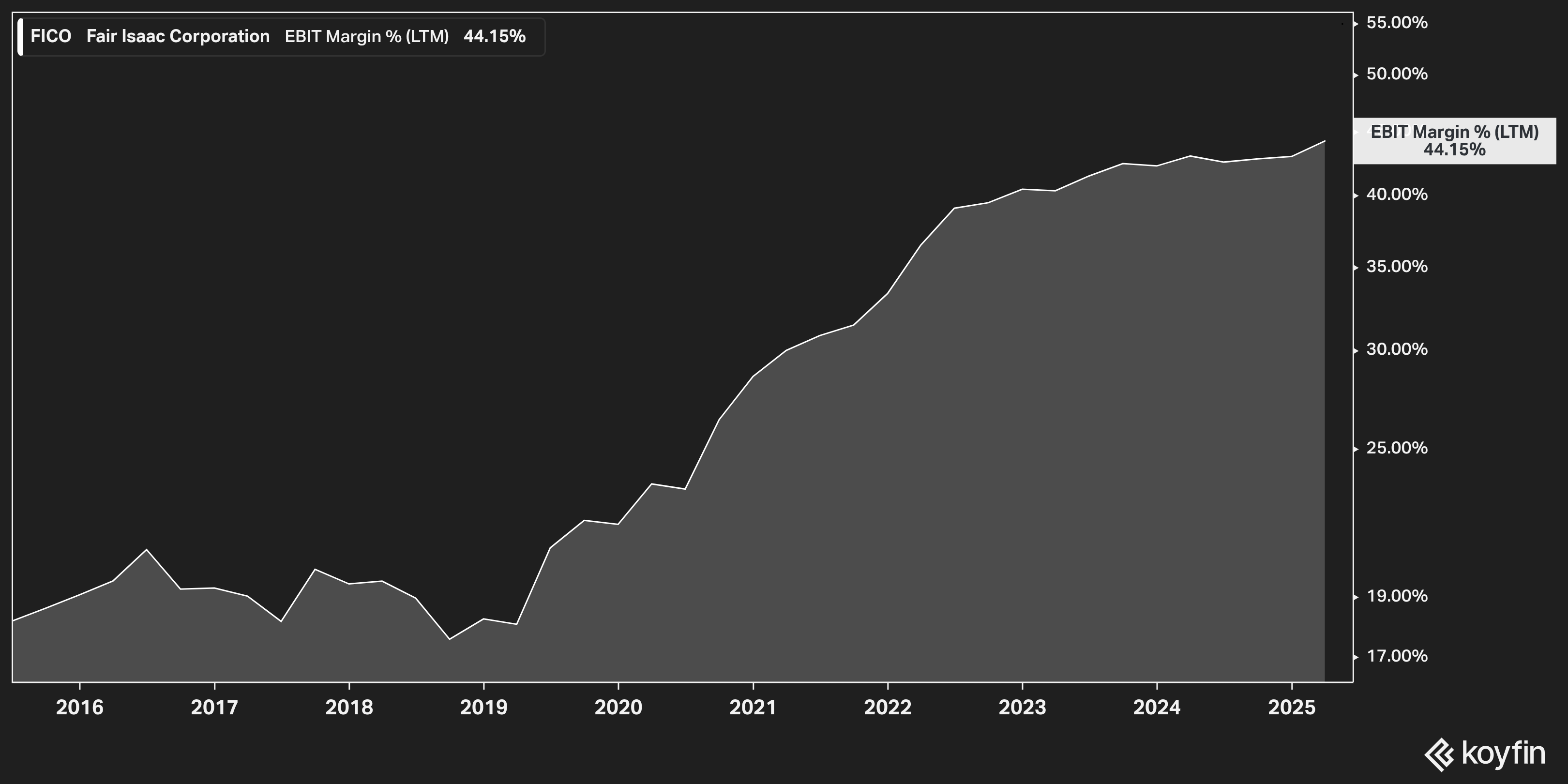

Operating margins have expanded from 25% to nearly 40% over the past several years. When you control critical infrastructure, you can do that.

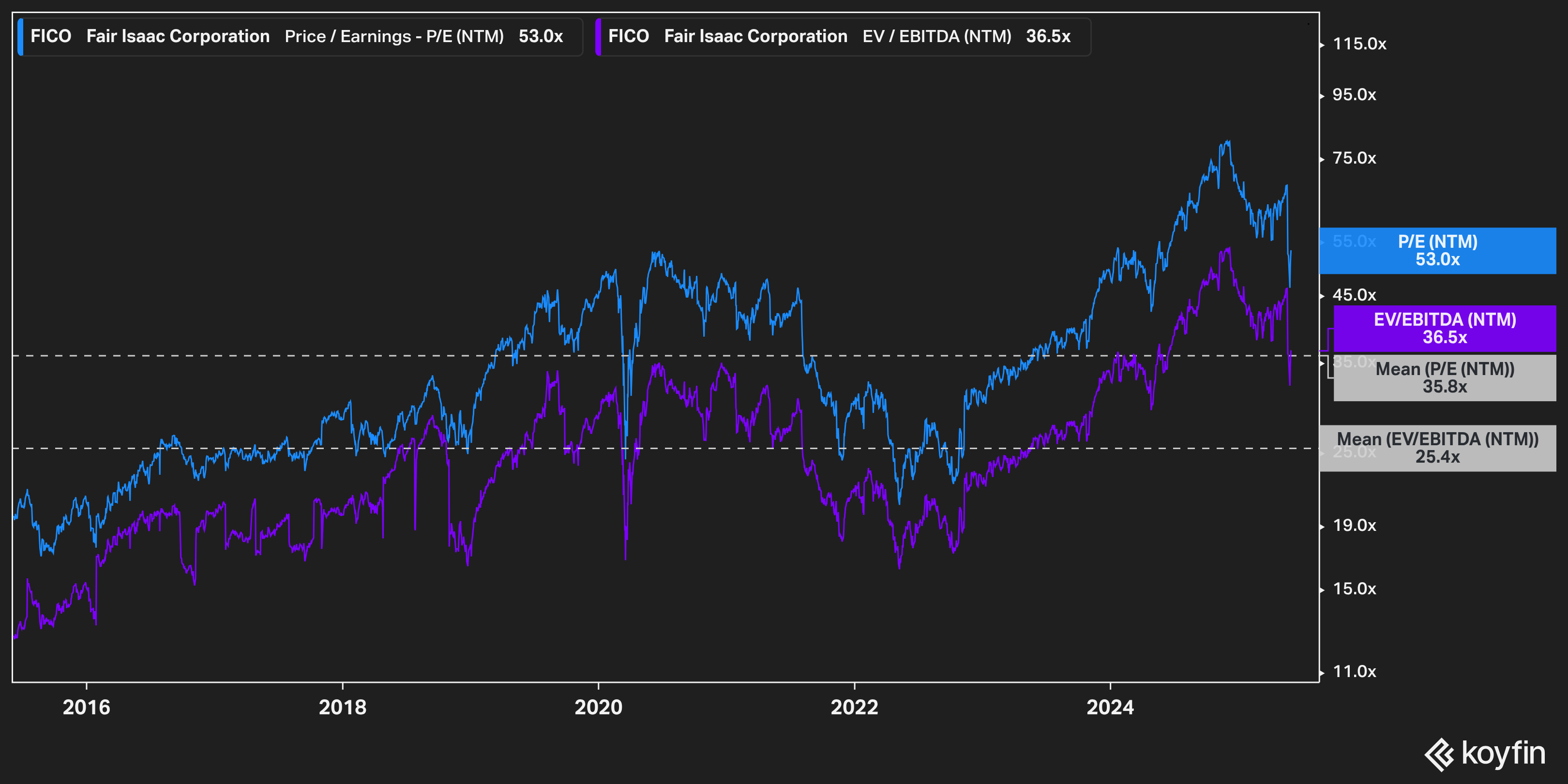

But even after this recent pullback, valuation remains the sticking point. We're paying 50-60x earnings for a company with a 36x historical average. The business quality justifies a premium, but this much?

The Risks:

The growth rate doesn't match the multiple, and rising interest rates could slow mortgage originations, which hits their bread-and-butter scoring revenue.

The company also faces growing regulatory scrutiny from the CFPB, which has called out credit reporting costs as excessive and is exploring potential rulemaking.

Copart ($CPRT) - The Salvage Auction King

Every time someone crashes their car, floods it, or gets caught in a hailstorm, insurance companies need to get rid of the wreckage. Copart runs the marketplace where they sell these cars to rebuilders, exporters, and parts dealers.

They've got 200+ locations across 11 countries and handle over 2 million vehicles annually.

This is one of those rare businesses where the competitive advantages keep widening. Their auction sites require massive real estate footprints and regulatory approvals that take years to secure. Meanwhile, their VB3 virtual bidding technology lets buyers bid from anywhere in the world, expanding their buyer base while competitors are stuck with local bidders.

International expansion is where this gets interesting.

They've cracked the code in the U.S., and now they're rolling out the same playbook globally. The UK business is already profitable, and they're making moves in Germany and other European markets. Vehicle density is higher overseas, accident rates are similar, and local competitors are fragmented mom-and-pop operations.

The unit economics are beautiful. Once they acquire a yard and build out the technology infrastructure, incremental volume drops straight to the bottom line.

Revenue per vehicle has grown from $400 to over $700 in the past decade, driven by higher car values and increased international buyer participation.

The stock has pulled back about 19% from recent highs, which creates an interesting entry point for a business that rarely goes on sale. The decline seems tied more to sector rotation than any fundamental issues with the business itself.

Even after the pullback, this isn't exactly cheap. At roughly 31x earnings, Copart trades at a premium to most industrial businesses, though the multiple has compressed from higher levels.

The Risks:

This is a cyclical business wearing a growth stock costume. When car values drop (like they did in 2008-2009), revenue per vehicle falls hard. If people drive less or buy fewer cars, accident rates decline and inventory dries up.

Management also has a history of aggressive accounting around revenue recognition that makes me occasionally squint at the numbers.

Occidental Petroleum ($OXY) - Buffett's Energy Bet

OXY is an oil and gas company with significant operations in the Permian Basin, plus some international assets and chemical operations. They're differentiated by their enhanced oil recovery techniques and, increasingly, their carbon capture technology.

Two words: Warren Buffett. Berkshire owns over 28% of the company now, and Buffett keeps buying more. When the world's best capital allocator backs up the truck on an oil company, I pay attention.

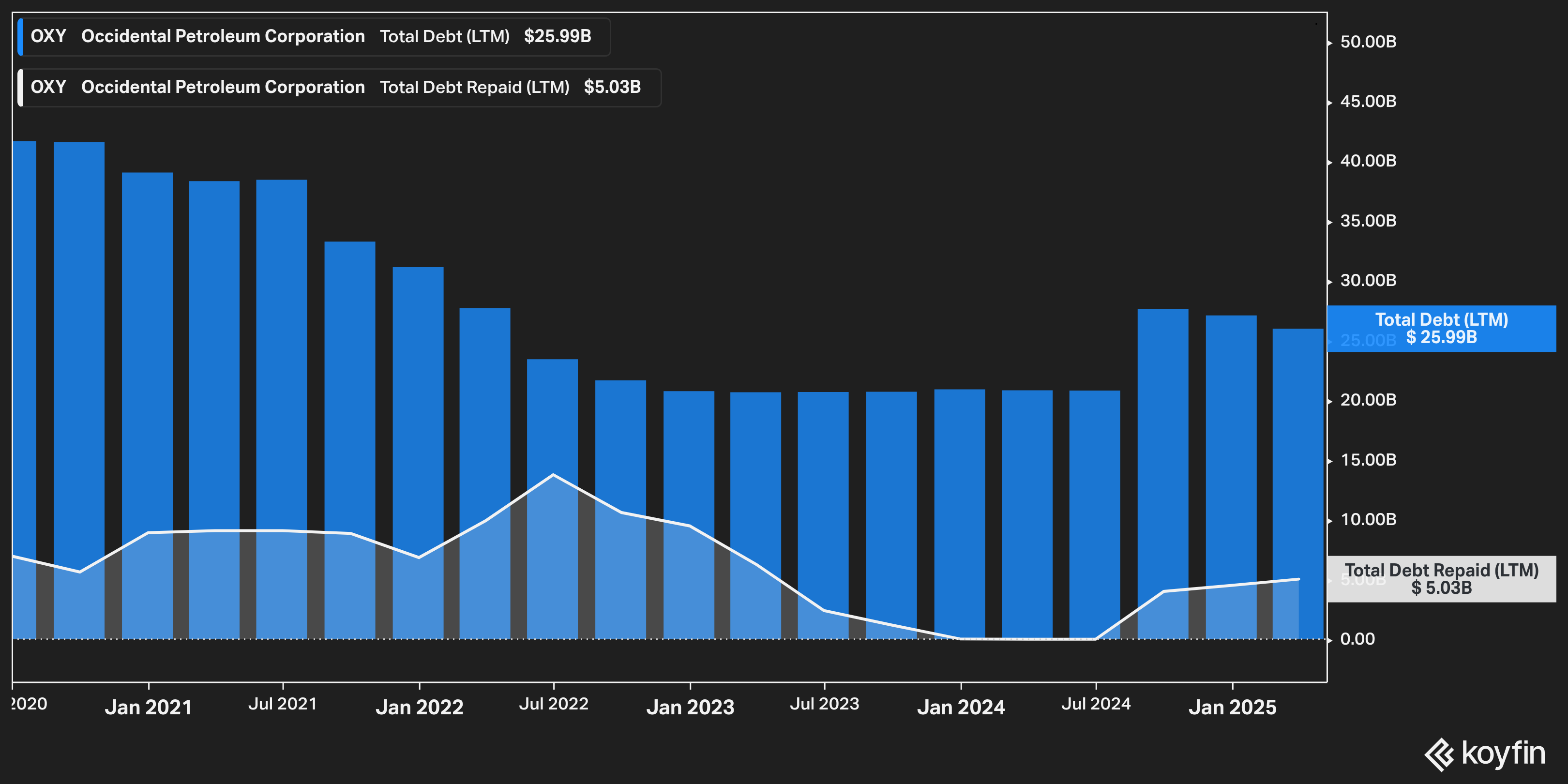

The transformation story is real. Five years ago, OXY was a leveraged mess trading near bankruptcy levels.

They've since made major progress on debt reduction—hitting their $4.5 billion target seven months early—while generating massive free cash flow.

But here's the wild card: carbon capture. OXY operates the world's largest direct air capture facility and has plans for much bigger ones. If carbon credits become valuable or governments start paying for carbon removal, this could separate OXY from being just another oil company.

Early innings, but the optionality is real.

The stock has been hammered, falling over 44% from its peak as oil prices softened and energy stocks fell out of favor. Even Buffett's continued buying hasn't been enough to stem the decline, though it does suggest he sees value at these levels.

The selloff has made the valuation more compelling. Energy stocks trade at historically low multiples, and OXY is no exception. At current levels, you're getting significant free cash flow generation at a reasonable price, assuming oil doesn't crater.

The Risks:

You're still betting on oil prices, and management has a questionable track record. They bought Anadarko at the worst possible time in 2019, loading up on debt right before the pandemic crashed oil prices. The CEO talks a good game about capital discipline, but the track record suggests otherwise.

ESG headwinds aren't going away either. Institutional investors are reducing oil exposure, and financing for new projects is getting tighter. This creates opportunities for existing players but also caps long-term growth potential.

The Bottom Line

Three very different businesses, three different risk profiles.

FICO offers defensive growth at a temporarily discounted price, Copart provides exposure to an irreplaceable marketplace with global expansion potential, and OXY gives you Buffett-endorsed energy exposure with carbon capture optionality.

None are obvious buys today, but all three are building compelling cases. I'm watching for better entry points and hoping the market gives me a chance to buy quality businesses at reasonable prices.

What stocks are catching your eye lately? Drop a reply—I read them all

Until next time,

Brian

Disclaimer: This is not investment advice. I may have positions in any securities mentioned. Do your own research, and remember that most "radar" stocks should stay on radar.

would love to own fico below 30x