[Update] British American Tobacco (BTI)

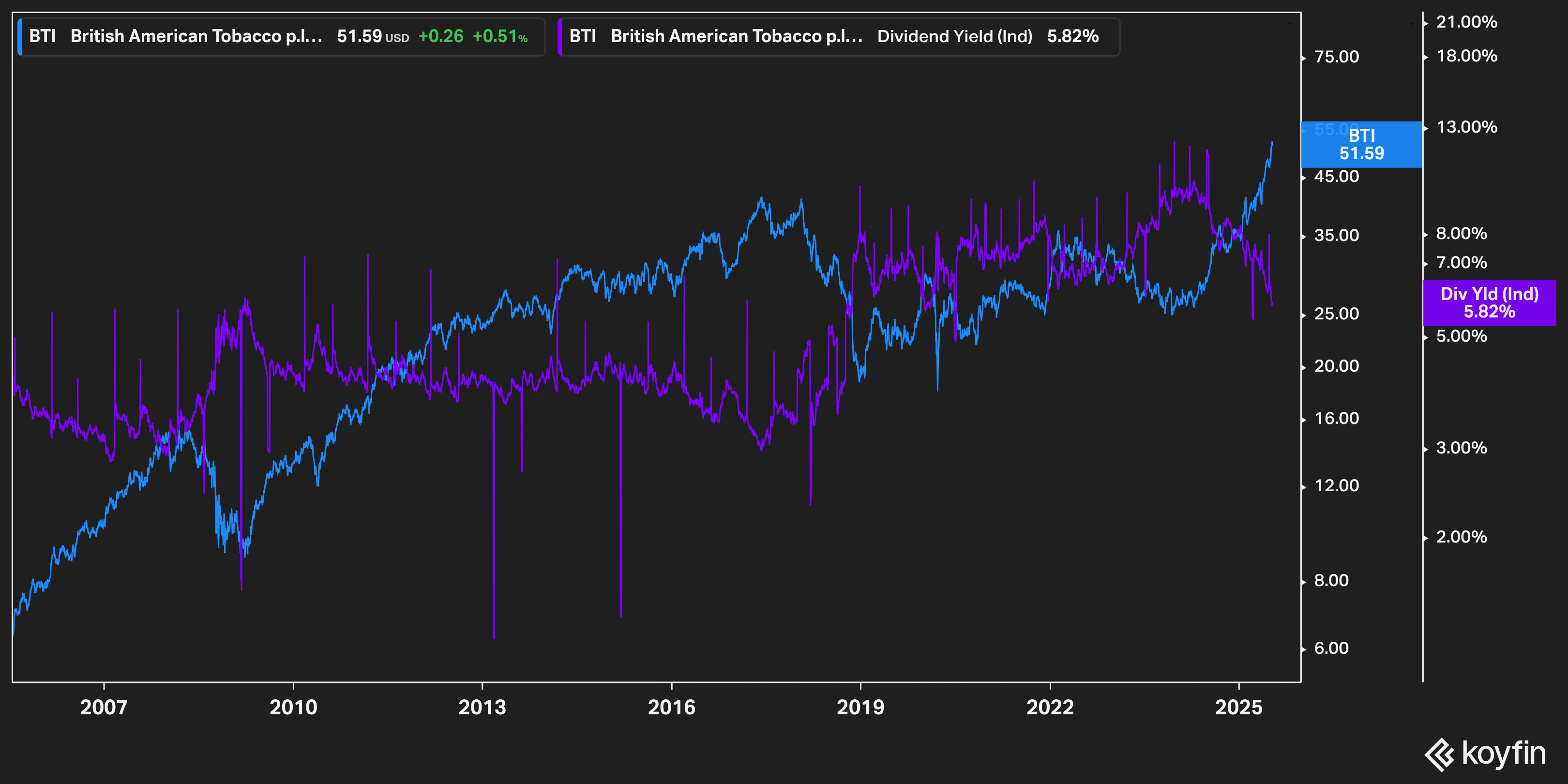

The stock has climbed nearly 50%, the dividend yield has compressed to about 6%, and investor sentiment has clearly shifted.

Before jumping in, here’s a link to my original BTI deep dive from March—

worth a look if you want the full background:

When I first wrote about BTI a few months ago, it felt like no one wanted to touch the stock.

The narrative around it was tired: regulatory uncertainty, declining cigarette volumes, a struggling U.S. business, and years of underperformance from its smokeless portfolio. Despite throwing off plenty of cash, paying a nearly 8% dividend, and buying back shares, the stock couldn’t catch a bid.

Back then, the stock traded at just 8x forward earnings and 7x free cash flow. Meanwhile, Philip Morris (PM)—with similar financial characteristics—was priced at over 20x earnings and 20x FCF. That kind of gap wasn’t about fundamentals. It was sentiment.

My view at the time was simple: BTI wasn’t broken. It was mispriced. Concerns around menthol regulation, Canadian litigation, and New Category profitability were weighing on the multiple—but most of those issues looked temporary and manageable.

Fast forward to today, and BTI is sitting at a new all-time high.

The stock has climbed nearly 50%, the dividend yield has compressed to about 6%, and investor sentiment has clearly shifted. The business hasn’t changed overnight, but the clouds have cleared, and what’s left is a far more stable and attractive setup than the market previously recognized.

From Clouded to Clearer: A Healthier Business Narrative

By early 2025, the regulatory and legal overhangs that had weighed on BTI for years were finally starting to lift. One of the biggest was the FDA’s long-delayed menthol cigarette ban, which had posed a serious threat to Newport—BTI’s flagship menthol brand in the U.S.

After years of delays and mounting political pressure, the proposal was officially withdrawn in January 2025 by the incoming Trump administration. At first, the market didn’t respond much. But as the dust settled, it became clear that a major risk to BTI’s U.S. cash flows had quietly disappeared. With that uncertainty gone, Newport’s future looked a lot more stable—and so did the outlook for BTI’s largest profit center.

Just a couple of months later, in March, another longstanding issue was finally resolved. A Canadian court approved the long-stalled litigation settlement involving Imperial Tobacco Canada. BTI had already provisioned £6.2 billion for the case, but the lack of resolution kept investors uneasy. The final terms confirmed that payments would be made gradually through future Canadian earnings—not through a sudden hit to the balance sheet. With that ruling, another weight came off the stock.

These back-to-back developments didn’t fundamentally change the business, but they removed two of the biggest question marks hanging over it. Once those clouds lifted, investors could finally focus on what BTI was actually delivering—and what was starting to work.

Velo and the Shift Toward a Smokeless Future

Of everything that’s changed for BTI over the past year, nothing has had more impact than Velo.

Keep reading with a 7-day free trial

Subscribe to Coughlin Capital to keep reading this post and get 7 days of free access to the full post archives.